The 2019-20 release of financial data from HESA offers us the first chance to look at provider finances during the pandemic.

It’s not a perfect view by any means – the massive pensions adjustment that plunged many universities into the red last year has wound back, so in some cases an unexpected improvement year on year is just a regression to the underlying trajectory. HESA usually provides a set of Key Financial Indicators alongside this release, but for 2019-20 data this will turn up in August, following the data manipulations required to account for the pensions issue.

And we don’t really learn anything of value about fee income. The major source of provider income would largely have been based on recruitment in the 2019 cycle and earlier, so we won’t see any information of value there until this time next year.

Is credit crunching?

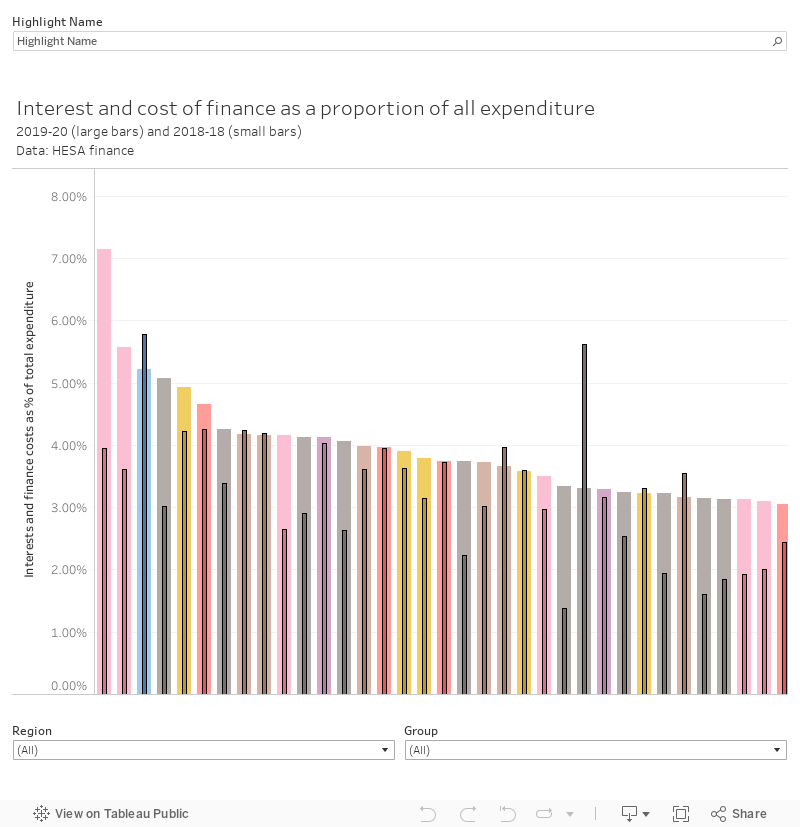

One thing I have been keeping an eye on is borrowing. Many providers set up additional borrowing facilities over the last year, some employing short term facilities (including the government-backed facilities) not often used by the higher education sector; in general UK HE has access to longer-term borrowing on favourable terms.

Though there are some figures available on the amount of borrowing, these are usually riven with definitional issues, and would not tell us what kind of borrowing is being used. Instead, I’ve plotted the interest and the cost of finance as a proportion of all expenditure for each of the last two years. This does not include the costs of paying down the principal sum of the loan, just the interest and other charges.

Interest and fee payments are something providers largely want to avoid – this is money that could otherwise be used to pay staff or improve facilities. A sharp year on year rise may suggest that a provider is taking on the kind of debt it would prefer not to make use of in normal times – but the figures for Cambridge (at the top of the chart for 2019-20) shows instead the cost of some fairly hefty (and complex) long term borrowing and investment plans.

However, sharp growth in other providers is most likely indicative of short term finance. Clearly not everyone has the kind of reserves available to Cambridge – and finance directors will not be happy about the way this indicator has drifted up. If you are wondering about the University of Northampton, which has the borrowing underpinning an entire new campus to think about, data was not finalised in time – though a look at its annual accounts suggests that this ratio remains similar to last year’s sector-leading 8 per cent of all expenditure being on the costs of finance.

Where borrowing costs have ticked up, there will be a huge incentive to pay short-term borrowings back as soon as possible. These interest rates will be higher than those associated with long term debt, and the period for repayment will be correspondingly shorter. Having long term commitments alongside this just exacerbates the issue.

Checking in before the drinks reception

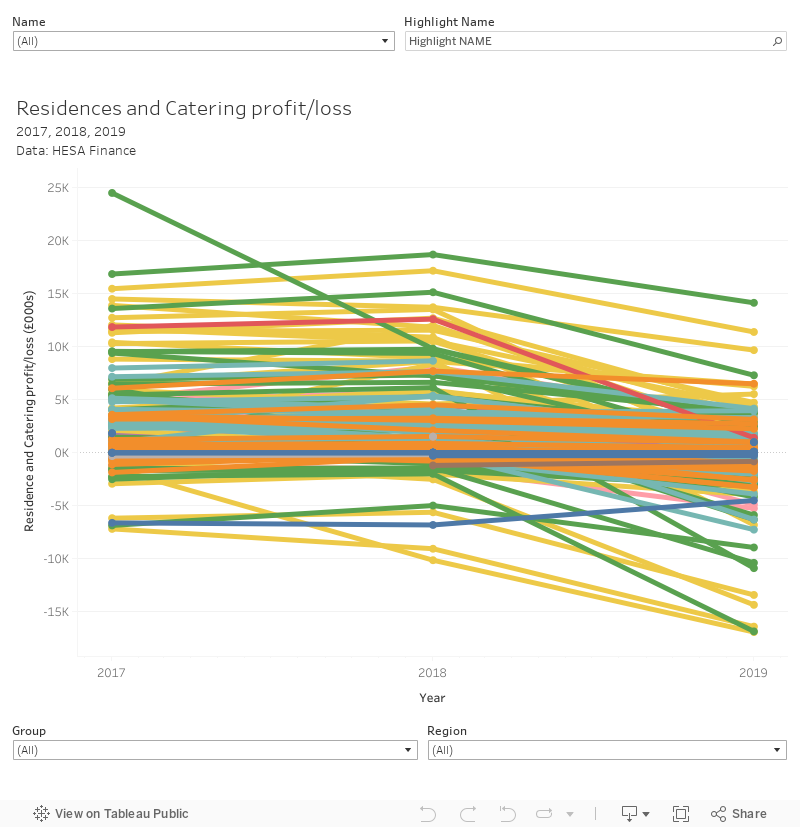

I’m also interested in what we see when we look at expenditure and income on residences and catering. During wave one of the pandemic, the sector pivoted to remote learning – with most students returning to their home address, and very little activity taking place on campus. This lack of activity extended to the often remunerative conference and events sector, a major source of income for many providers outside of term time (and in some notable cases all year round).

Bear in mind that for the majority of the year (September through to March) there was no change to normal patterns, but that Easter and summer – both key conferencing periods – were affected Here’s a plot of changes over three years, for each provider.

The general trend is negative, but is particularly pronounced in a handful of Russell Group and other pre-92 providers. The universities of Sheffield, Reading, and King’s College London all made a loss of around £17m on catering and residence activity in 2019-20.

Pay your staff right

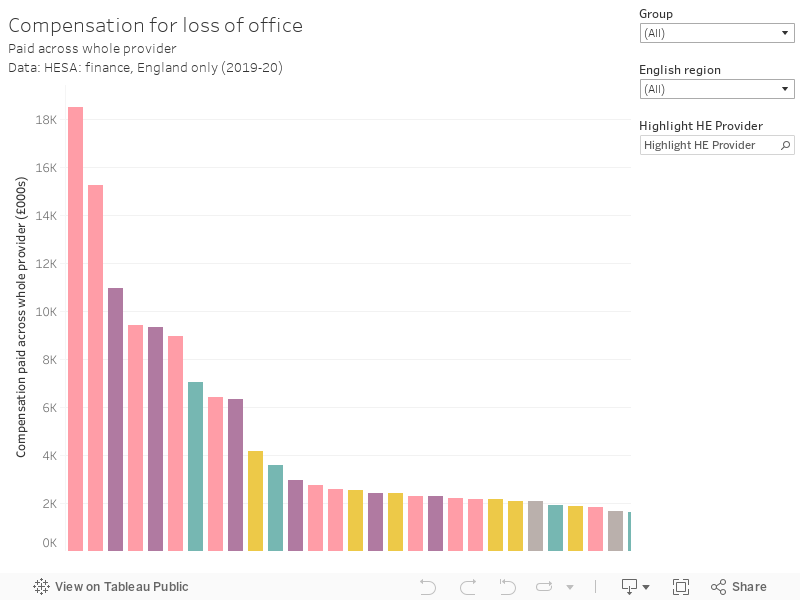

Eight hundred and seventy staff at the University of Manchester received a payment as compensation for loss of office in 2019-20, a share of £18.5m. At the University of Nottingham 544 staff shared £15.2m. Across the whole English sector, £183.3m was spent on compensating staff for loss of office. Figures like this remind us that doing redundancies and related end-of-job processes properly and equitably is a hugely expensive business.

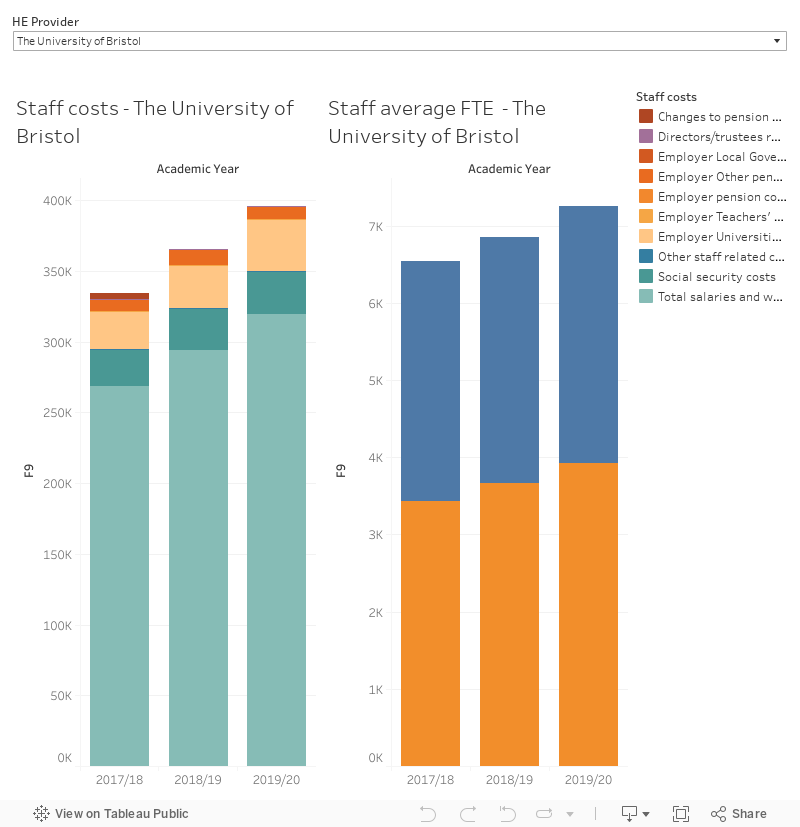

We also see data on costs associated with staff that are still employed by a provider. I’ve only presented data since 2017-18 (with the full breakdown of pension costs) – and FTE for academic and non-academic staff are on the right. This is a new addition to the data set – but the old way of looking at this (with less granularity over costs but the ability to filter by cost centre) is there too.

The trend is generally stable or rising, but not all providers have returned the data that underpins this chart, so don’t be surprised if information is missing.

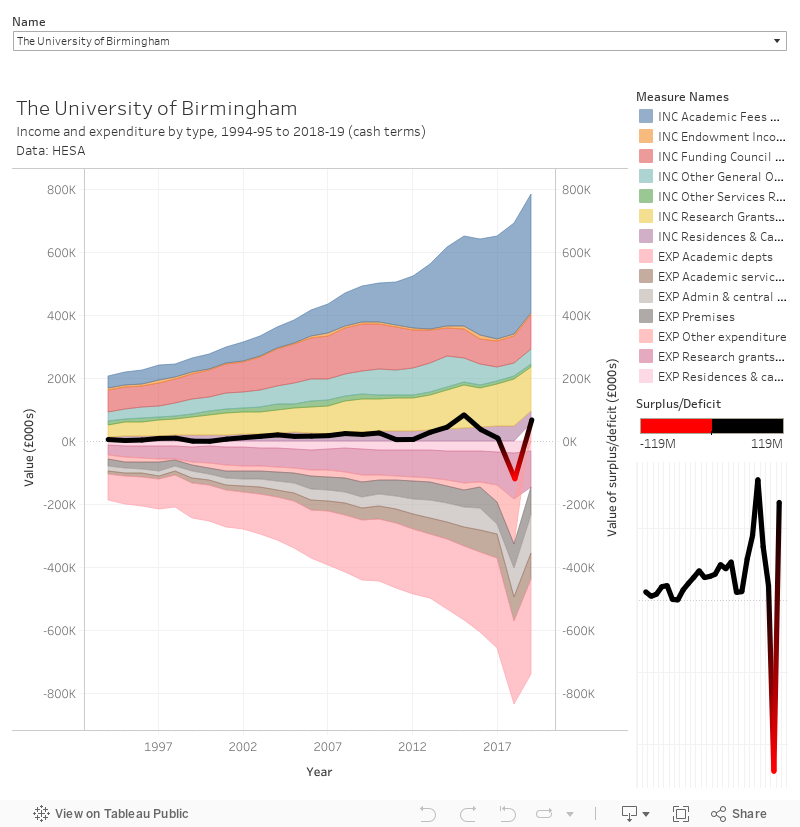

Long term trends

For many, but not all providers, I now have an income and expenditure time series going back 25 years. These figures are in cash terms (so don’t take inflation into account) – but have proved popular in the past so I’m happy to update them.

You can see that, as Andrew Connolly predicted on the site last year, the USS-based “losses” last year have become “gains” in this year for many established providers (do read the piece, it is a complex area).

Thanks, David – useful analysis as ever. I think the charts on staff costs and staff average FTE need a tweak in Tableau. I think the right hand chart of FTEs needs to be using the using the average of the data, not the sum.

Cheers Andrew – I actually needed to set HESA’s strange country and region global filters to “all” for that graph. Now done.