There’s not many in the higher education sector that would have welcomed any part of the recent immigration white paper.

The reduction in the graduate route time limit would have been difficult enough. The BCA changes to duties on providers in order to sponsor international students will cause many problems. The possibility of financial penalties linked to asylum claims for those on student visas was as unexpected as it is problematic.

But it is the levy that has really attracted the ire of UK higher education.

The best form of defence

On one level it is simply a tax – on the income from international student fees, which is one of a vanishingly few places from which universities can cross-subsidise loss-making activity like research and teaching UK-domiciled students.

Yes, the funds raised are promised variously to “skills and higher education” or just “skills”, and the suggestion seems to be that the costs will be passed on entirely to international students via rises in tuition fees. There’s not any real information on the assumptions underpinning this position, or credible calculations by which the proportion of students that may be deterred by these rises and other measures has been estimated.

But details are still scant – the government has, after all, only promised to “explore” the introduction of a levy – and used the idea of a six per cent levy on international tuition fees as an “illustrative example”. We have to look forward to the Autumn statement (not even the skills white paper – remember joined-up, mission-led, government?) for more – and do recall that the white paper is a consultation and responses need to be made in order to finesse the policy.

Thinking about impact

There’s no reliable way to assess the impact of this policy with so little information, but we do know a lot about the exposure of each university to the international market.

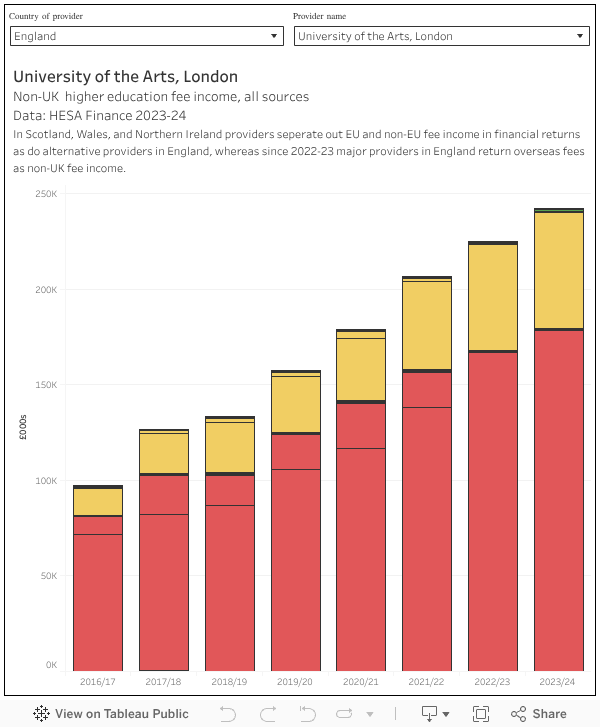

For starters here’s a summary of provider income from overseas fees since 2016–17 – both for individual providers and (via the filters) for the sector as a whole.

The story has been one of growth pretty much anywhere you care to look – with only limited evidence of a cooling off in the most recent year of data. Some institutions have trebled their income from this source over the eight years of available data, with particular growth in postgraduate taught provision.

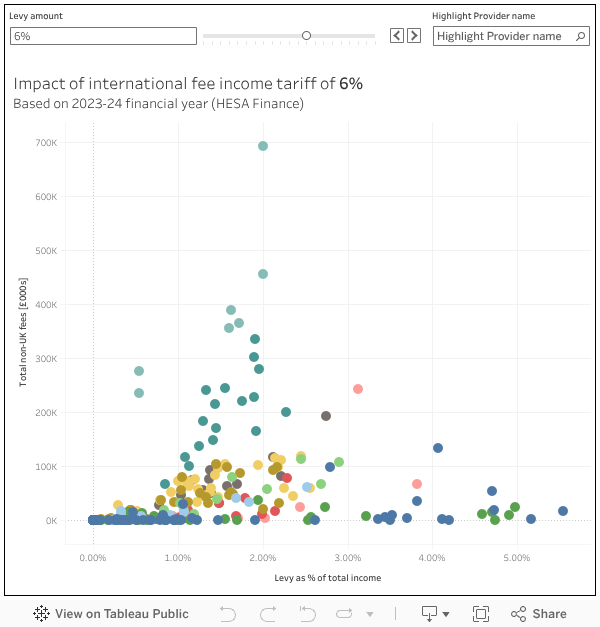

In considering the financial impact of a potential levy I have used the most recent (2023–24) year of financial data – showing the total non-UK fee income on the vertical axis and the proportion of total income represented by the value of the levy on the horizontal. By default I have modelled a levy of six per cent (you can use the filter to consider other levels).

Who’s up, who’s down?

In the majority of large universities the cost of levy is equivalent to around two per cent of total income. In the main it is the Russell Group that sees substantial income from international fees – the small number of exceptions (most notably the University of Hertfordshire and the University of the Arts London) would see a levy impact of closer to three per cent of total income.

What we can’t realistically model is university pricing behavior and the impact on recruitment. Universities generally charge what the market will stand for international courses – and this value is generally higher for providers that are better known from popular league tables.

Subject areas and qualifications also have an impact (the cost of an MBA, for example, may be higher than a taught creative arts masters – a year of postgraduate study may cost more than a year of an undergraduate course), as does the country from which students are arriving (China may be charged more than India, for example).

Some better off universities in the middle of the market may choose to swallow more of the cost of the levy in order to increase their competitiveness for applicants making decisions on price – this would put pressure on the currently cheaper end of the market to follow suit as well as direct competitors, and may lower the overall floor price for particular providers (though, to be fair, private providers are still better positioned to undercut should they have access to funds from investment or other parts of the business).

There is an obvious impact on the quality of the provision if providers do cut the amount of fee income – and this as well could have an impact on the attractiveness of the whole sector. For more hands-on courses in technical or creative subjects, provision may become unviable overall – surrendering the soft power of influence in these fields.

A starting point

It’s not often that we see a policy proposal on university funding launched with so little information. Generations of politicians have learned that university funding policy changes are the equivalent of poking a wasps nest with a sharp stick – it may be something that needs doing but the short term pain and noise is massive.

It could be that it is a deliberate policy to let the sector (and associated commentariat) go crazy for a month or so while a plan is developed to avoid the less desirable (for ministers) consequences. But the idea that international students will gladly pay more to support an underfunded sector is one that has been at the heart of university activity for decades – the only real change here is that the government feels it can put some of the profits to better use than some of our larger and better-known providers.

In all of this there appears to have been little consideration of the fairness of putting extra costs onto the fees of international students – particularly where they personally don’t see any value from their additional spend. But this has been an issue for a good few years, and it seems to have taken the possibility of a tariff (which could be considered unfair to cash-strapped universities too) to drive this problem further up the sector’s agenda.

Without accepting that there is any justification at all for this policy, if the government insists on applying this then it can surely only be applied to new students, and from 26-27 at the earliest (otherwise how can institutions even consider passing costs on to students?) And if they are talking about real “income” then they should subtract costs of acquisition from fee income: scholarships and fee discounts, agent fees, costs of running overseas offices… But perhaps they haven’t completely thought all of this through?