With calls for a sector specific Covid-19 bailout rebuffed by government, imagine if the same week saw news of a cut in state funding for teaching?

That’s pretty much what has happened in England, with OfS announcing the results of a consultation that began following January’s guidance letter from Gavin Williamson requesting a £70m cut in recurrent teaching funding for the 2020-21 financial year (April to March). Running between mid-January and mid-February, the consultation sought sector feedback on proposals developed by the regulator regarding the fairest way to share the pain.

To say this isn’t a great look right now is perhaps to understate the issue a little. The sector was given no justification for the government decision to make these cuts – it felt arbitrary at the time, but right now it just feels petty. The sums involved are not, in the grand scheme of things, large, but the timing makes OfS look bad – unfair given that it was not their decision.

Money, off

Twenty-six million pounds will be shaved off sundry funds not yet committed for the 2019-20 academic year, with a reduction of £48 million planned for the 2020-21 academic year. The biggest chunk of these later cuts will come from support for high-cost teaching – £33m from the various elements that support this.

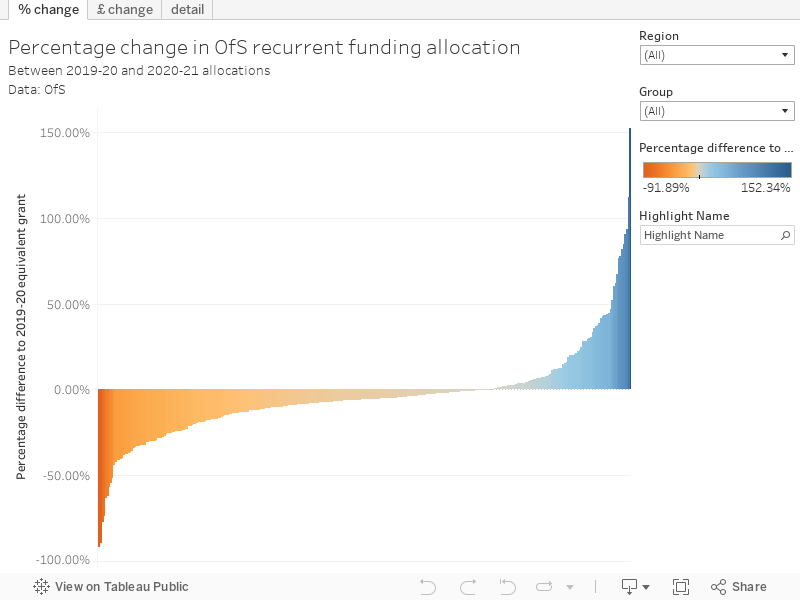

On 13 May OfS published details of these funding changes at a provider level. What doesn’t come through at a sector level is that the pro-rata nature of many of these cuts, plus increases in student numbers in high cost subjects, means that a fair few providers see funding increases for 2020-21. I’ve three graphs for you here on the tabs – the percentage change in funding between this year and last year, the change in cash terms, and a full break down of funding by type. The latter has a “Name” filter allowing you to look in detail at institutional allocations.

In such times it is good news that the rate of funding for nursing, midwifery, and allied health are preserved. As a large orange box makes clear, this settlement was developed before the onset of the coronavirus became clear. There’s latitude for OfS to keep funding decisions under review during and after the pandemic, although DfE has not exactly been forthcoming with sector funding so far.

The big hit is on high-cost subject funding, with students studying subjects that fit within price groups A, B, and C1 (the only students that attract this funding) seeing an across-the-board cut of 5.2 per cent per FTE. As above, nursing, midwifery and allied health sees an exemption to this via a corresponding top up to their supplement.

For the most cut-throat recruitment round in living memory, there’s a £16m cut from access and success budgets, falling entirely on student premiums for full-time and part-time undergraduates. Uni Connect and disabled student premiums remain at their current values – as does funding for world-leading specialist providers.

Support for national facilities and regulatory initiatives will drop by £19m – a cut in funding for Jisc of £13 million, and £6m from OfS’s competitive funding programmes. Funds for Jisc were in the process of being reprofiled anyway – historically funding for the sector technology body came from the teaching grant even though much of the work of Jisc has been focused on research, so there’s a new split between OfS and Research England funding.

All of these adjustments were expected to prefigure a wider consultation on the OfS funding method, which has been delayed due to Covid-19. Four paragraphs bring us up to speed on this – we are still awaiting the response to the Augar review and any changes to HE funding that comes about because of decisions made here. This government response is still awaited alongside the next spending review – which is postponed for the duration, so a new funding method will emerge for the 2022-23 academic year at the earliest.

The one bright spot in all this is capital funding – there’s a small rise (£136m to £140m) for providers and an extra £10m for Jisc in the 2020-21 academic year; providers may also have seen small increases based on this year’s under-registration. A little bit of the available provider funding is held back for the interim for providers that may join the sector before March 2021, and to support development costs for Jisc and HESA for the Data Futures programme.

Down your way

That’s the funding implications set out, but the really interesting bit of this publication is the summary of responses to the consultation. This gives us an insight into sector priorities (if you cancel out the general overarching wish of the sector to be given as much money as possible with as few strings as possible).

All these cuts, of course, came shortly after providers were required to submit five year financial forecasts to OfS – those same forecasts that will now control 2020 student numbers. Of course, OfS could never have predicted the impact of Covid-19 – but it is unfortunate timing to say the least.

Ninety three percent of the 108 responses approved generally with the proposed approach, so we should not be surprised to see little difference between that and the plans outlined above. Providers were keen to avoid changes to amounts already budgeted this year, but noted that loading the bulk of the cuts into next year would adversely affect students.

General concerns were about cuts to Jisc resulting in worse services (problems with Janet connectivity or cyber security) or the cuts being passed on by Jisc via increased subscription fees (a Jisc spokesperson has since confirmed that 2021 subscription prices have already been set, and will not pass on this cut to members). OfS’s own running costs were also raised – the slightly cheeky response that OfS’ running costs are covered by subscriptions isn’t, strictly speaking, true (OfS gets about a third of its £27m income from DfE, including funds to run the ever-popular TEF).

Providers still care about the unit of resource – an idea that first saw sustained policy attention in the eighties, but became largely irrelevant in most cases since the move to majority fee funding in 2012. I say largely because for high cost subjects outside of healthcare the cuts may mean that providers are simply unable to offer as many student places. A few responses drew on the KPMG analysis that accompanied the Augar review (and failed to justify the £7,500 fee levels).

There was general approval for the allocation to “world class” specialist providers – probably largely from specialist providers. Other smaller providers are clearly keen to join this very short list, but have not been able to since the last review was conducted in 2015-16 before many had even entered the state-funded HE sector. We also see widespread love for Uni Connect, with only one party pooper noting that this funding was due to end in 2020-21 anyway.

A capacity issue?

Medical education is a complicated beast at the best of times – and it has been noted that even though the budget has been maintained and places available expanded, cuts to budgets for salary costs for clinical stuff could lead to a reduction in capacity.

And the London premium remains the massive headache it always was – providers in London agree with the concept but note that the costs of living in London have increased even further, while those outside London are not so keen. This is borne out here, though there is an interesting argument put forward that more students from deprived backgrounds study in London – although arguably the reduction in student premiums would have a greater impact here.

There was significant opposition to cuts to these premiums for underrepresented students – putting recruitment and support at risk (again, as it turns out, during a hellishly competitive 2020-21 recruitment that is likely to disadvantage such students anyway). It will clearly have a disproportionate impact on students in those groups – and will likely slow down progress on access and participation plans. A number of providers suggested the cuts would cause them to focus on international students and postgraduate students – something that looks pretty unlikely in retrospect. Smaller providers, and FE colleges, felt the cuts would affect them disproportionately.

Although the OfS has published “equivalent” 2019-20 figures, these are not exactly equivalent. There was also a methodological change to the way that the price group of activity has been arrived at (moved from module level to programme/course level).

Therefore changes in funding will disguise volume changes, method changes, as well as the -5.2% rate of funding change.