Live: Autumn Statement 2016

David Morris

Former Deputy Editor

David Morris is the Vice Chancellor’s policy adviser at the University of Greenwich and former Deputy Editor of Wonkhe. He writes in a personal capacity.

Updates

Autoload

Order

That’s it

The live blog is now over, we’ll continue to post analysis on the site today and tomorrow.

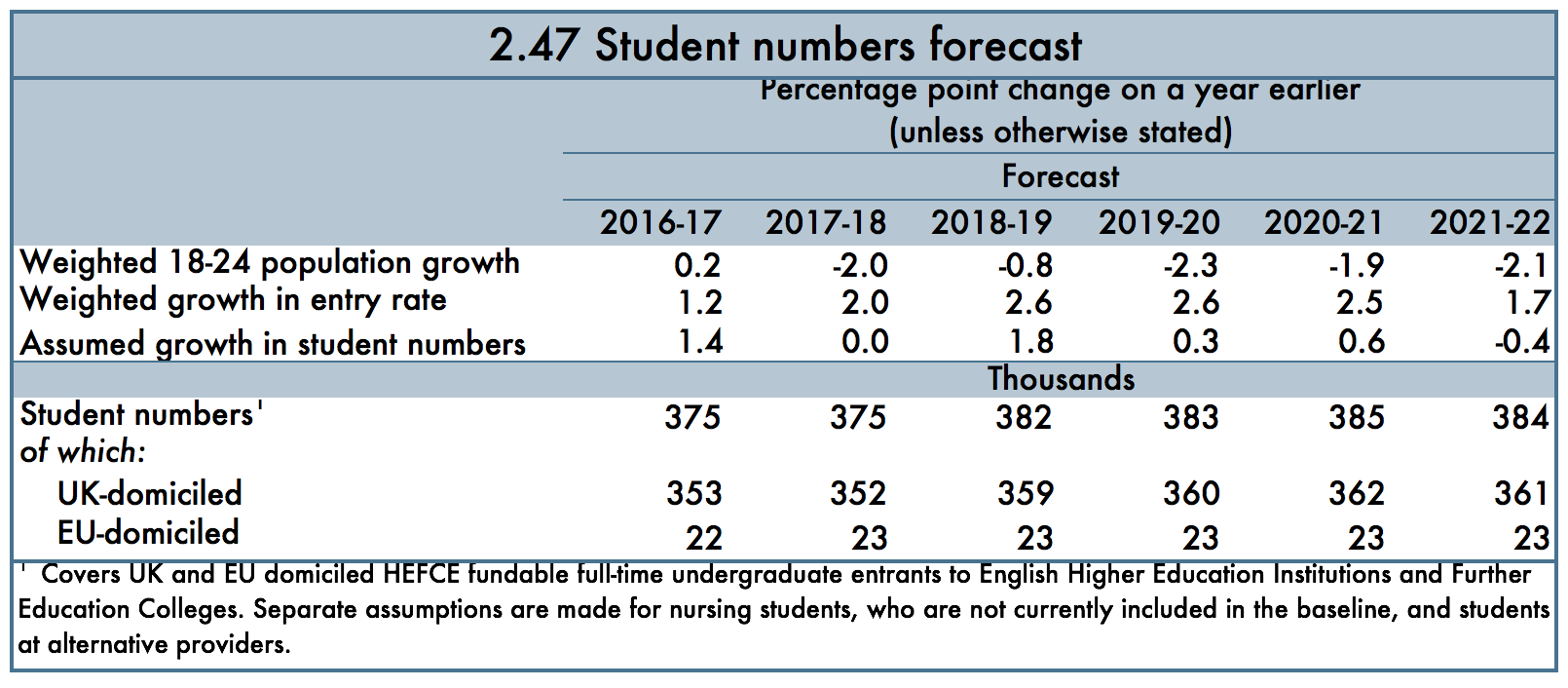

OBR projection for student number growth

As part of its calculations of national expenditure and receipts, the OBR has estimated student number growth and the overall position of the loan book. In contrast to English universities’ more bullish projections for student number growth, the OBR reckons on only minimal growth.

![OBR projection wonkhe student number]()

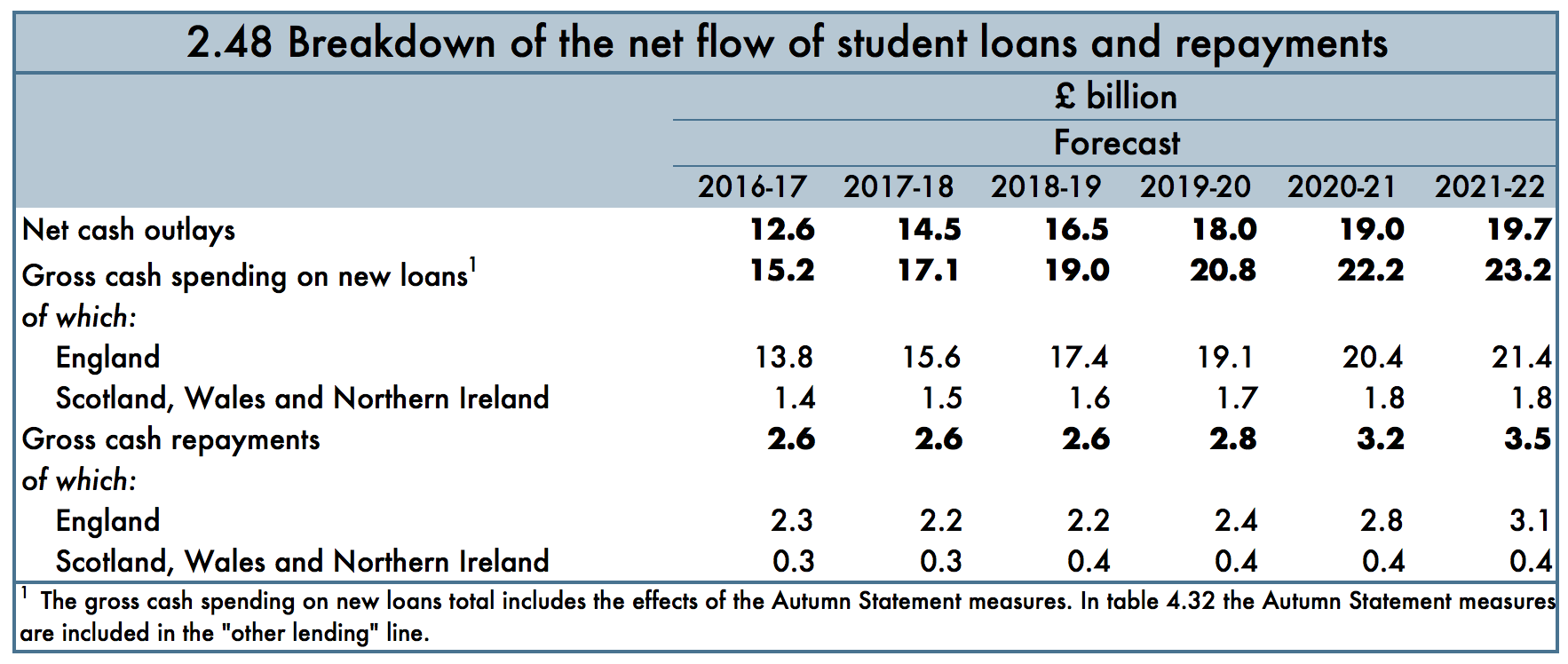

The net outflow of expenditure on student loans is projected to grow to reach nearly £20bn in 2021.

![obr projection wonkhe]()

You’ll note that the OBR has not included any figures for loan repayments from EU students, perhaps reflecting the difficulties the government has found in getting them to pay.

More on the new research and development fund

It appears that much of the new £2 billion for research and development really is new cash as part of the new NPIF, which will be funded through additional borrowing. The full Autumn Statement gives us some clarity on where it will be directed, though it looks like UK Research and Innovation will have a great deal of discretion over it. According to the statement, funding for the following will be included within the £2 billion:

• Industrial Strategy Challenge Fund – a new cross-disciplinary fund to support collaborations between business and the UK’s science base, which will set identifiable challenges for UK researchers to tackle. The fund will be managed by Innovate UK and research councils. Modelled on the USA’s Defense Advanced Research Projects Agency programme the challenge fund will cover a broad range of technologies, to be decided by an evidence-based process.

• Innovation, applied science and research – additional funding will be allocated to increase research capacity and business innovation, to further support the UK’s worldleading research base and to unlock its full potential. Once established, UKRI will award funding on the basis of national excellence and will include a substantial increase in grant funding through Innovate UK.

The government will also review the tax environment for R&D, and science and innovation audits will continue.

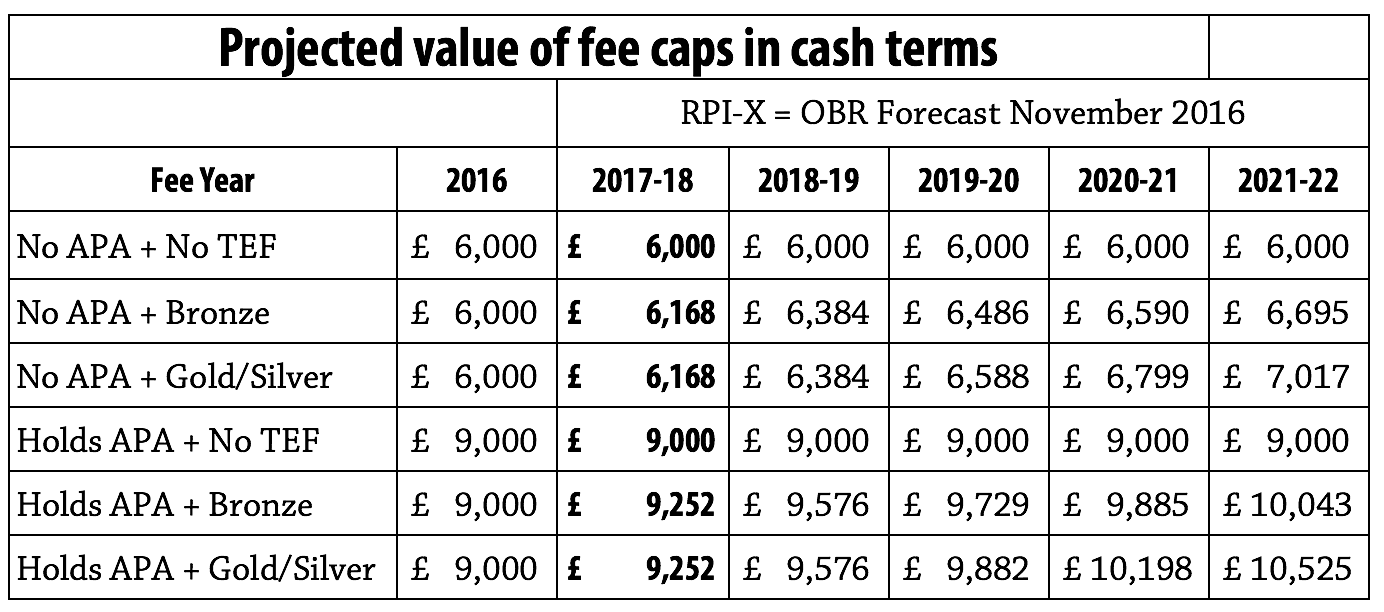

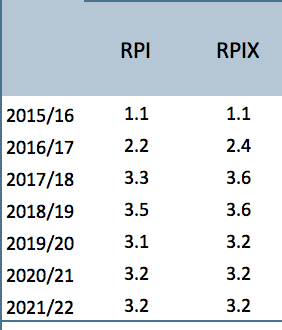

New fee projections

![wonkhe fees forecast]()

So following the release of the new RPI-X forecasts, we can now produce new projections for tuition fees forward to 2021-22. When discussing these projections with BIS (RIP) back in May, we were told that projections should be made based upon the Q1 forecasts within each academic year, so that is what we have done here.

If you read our forecast based on the March projections, you’ll see that the changes are not massive. Beyond 2018-19 RPI-X is only slightly higher than was forecast back in March.

HOWEVER, the big news here is how much universities will lose out in 2017-18. Back in May, Jo Johnson confirmed an increase of 2.8%, based on the OBR March forecast. The comparable figure for 2017-18 is now 3.6% – that’s a 29% difference. If fees were increased based upon today’s new forecast for 2017-18, they would be at £9,324 in 2017-18, a gap of £72 per student. That’s £1 million lost for a university with 15,000 undergraduates. This effect will compound into future years.

We should also exercise a healthy degree of caution about the OBR’s forecasts beyond 2018. The reversion to the mean in growth and inflation forecasts is effectively an admission by the OBR that they have absolutely no idea where in the economy will be in couple of years time, particularly as the Article 50 ‘cliff edge’ approaches. We simply just don’t know where inflation will be at by that point, but if Sterling continues its current trajectory then there is a safe bet that it will be even higher than forecast today.

*APA = Access and Progression Agreement

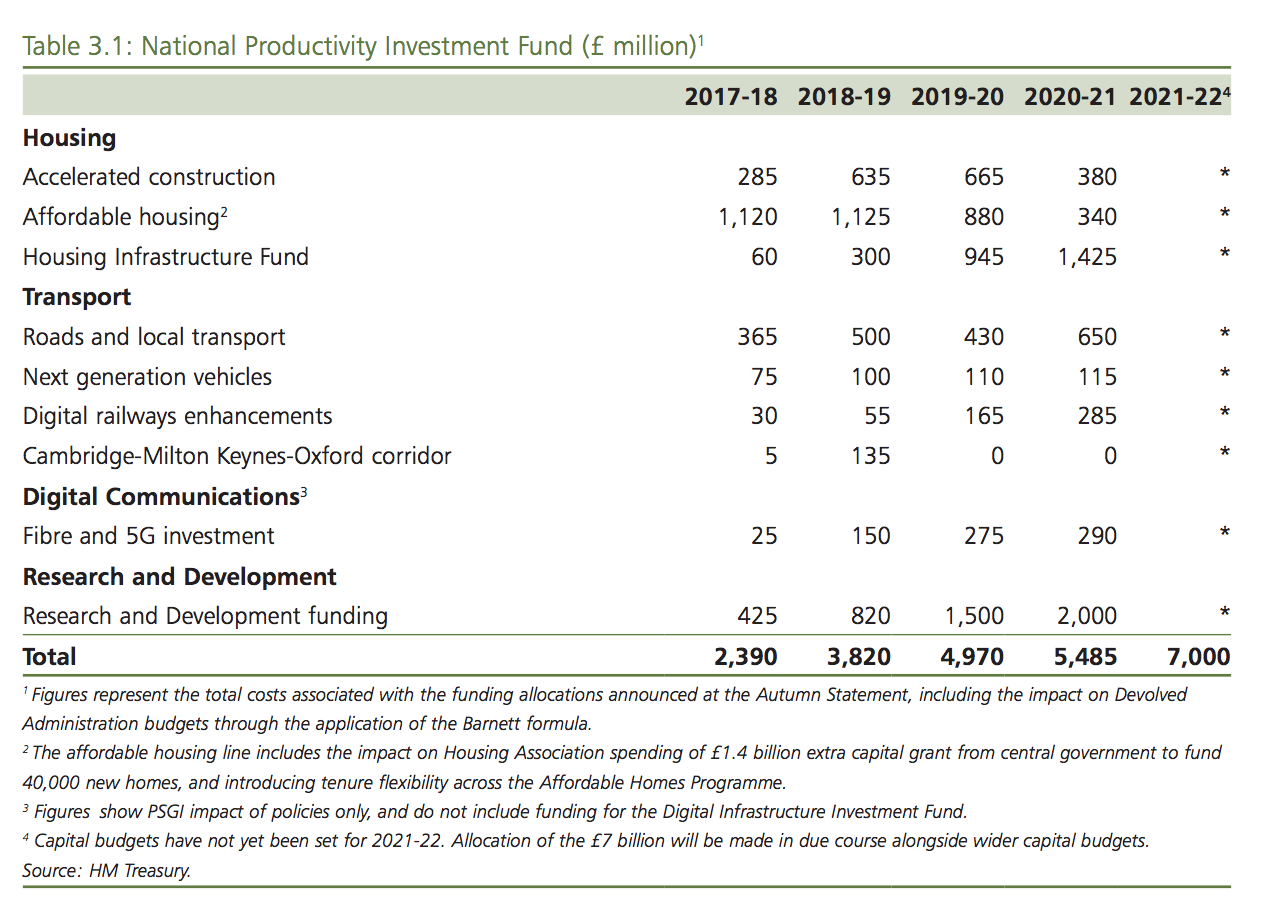

Increase in research spending: details released

We now a little more about how the new research spending will be phased in: an extra £425 million in ’17-’18, £820 million in ’18-’19, £1.5 billion in ’19-’20, and finally an extra £2 billion in ’20-’21. The funding compares well to other investments in the ‘National Productivity Investment Fund’.

![screen-shot-2016-11-23-at-14-12-39]()

Student loan sale delayed, again

The OBR confirm today that the sale of the student loan book is likely to be pushed back (again):

§4.168 we continue to expect the Government to raise around £12 billion from selling part of the pre-2012 student loan book. The timing of these sales has been pushed back in a number of forecasts and again in this forecast. The process of preparing for the initial sale tranche continues, but we now judge the probability that the first sale will be completed in 2016-17 to be less than 50 per cent. We have assumed that the first sale will be completed in early 2017-18, but that the Government will still be able to complete the second sale by the end of 2017-18. Uncertainty over these timings and the rest of the sale programme remains. Selling the loan book changes the years in which payments are received by

Uncertainty over these timings and the rest of the sale programme remains. Selling the loan book changes the years in which payments are received by government, with more recorded upfront as sales proceeds and less as loan repayments in future years, as these will flow to the private sector rather than the Exchequer.

Student loans and household income

There’s an interesting amendment to the way household incomes have been calculated within the Impact on Households document released alongside the Autumn Statement. Since the budget of earlier this year, student loans have now been included in household income figures, which aligns with the Office for National Statistics survey of Households Below Average Income.

The explanation is as follows:

2.29 To align with the definition of income used in the Households Below Average Income survey, the analysis of spending on public services also includes one financial transaction: student loans. To account for this source of income, estimates of student loan outlay in a given financial year are counted as household income from public spending. Likewise, estimates of student loan repayments in that same financial year are reflected as a loss to households, again through the public spending bars. Where a policy change affects the relative generosity of student loans, either by affecting the amount an individual can borrow, or the amount individuals will repay, this will be reflected as a change to household income.

Given the size of the student loan book in the context of the national accounts, this seems like a reasonable move. Though it would presumably have the effect of showing a large net increase in household income as the overall amount of student debt outstanding is projected to grow rapidly.

We speak too soon!

No sooner had we released the previous post, the OBR uploaded some more supplementary tables, and the RPI-X projections have indeed been released!

We’ll have a full update on the implications for TEF momentarily.

![screen-shot-2016-11-23-at-13-53-13]()

No new RPI-X forecast: implications for TEF

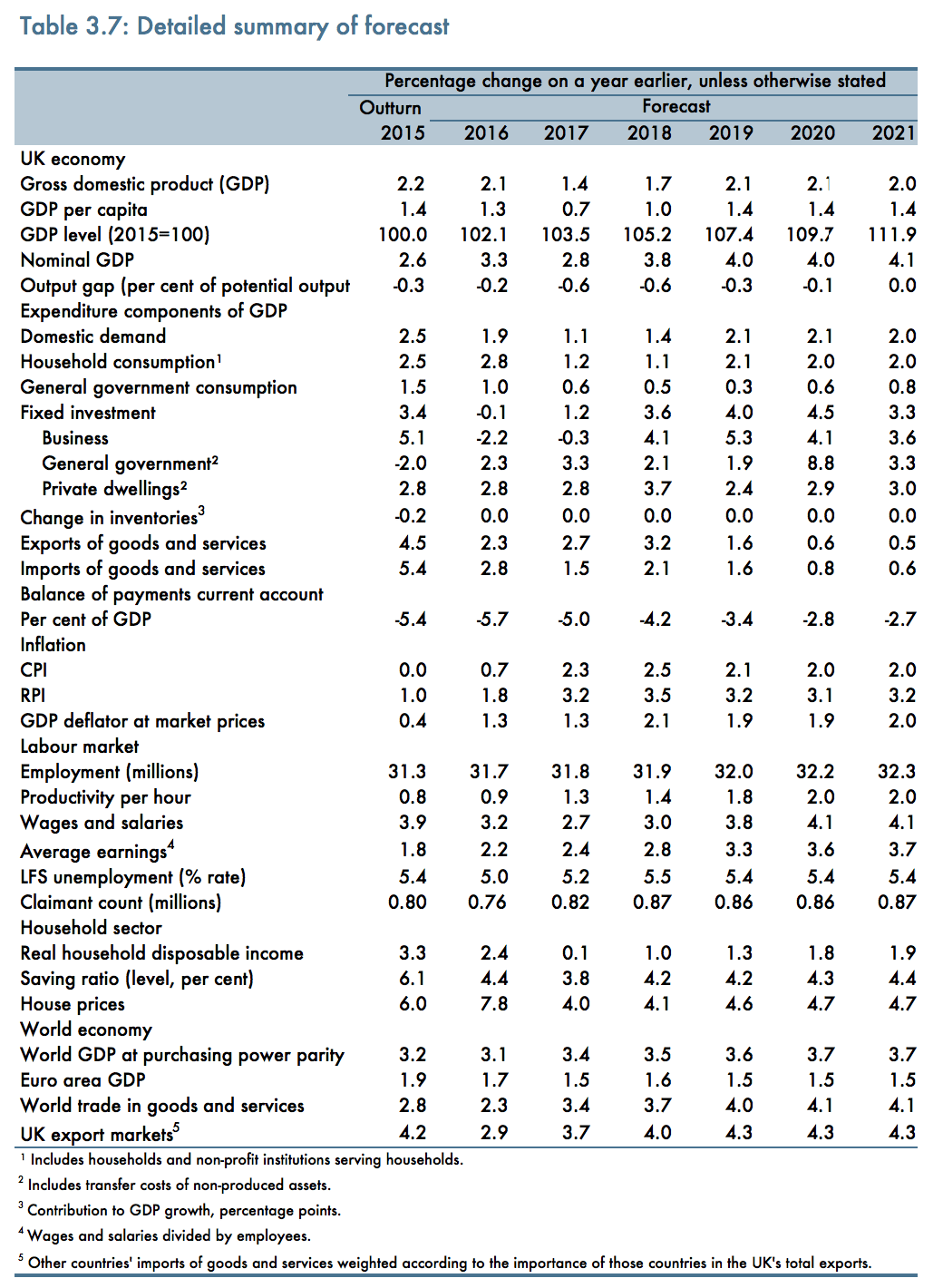

Now the real fun begins, with the detailed Autumn Statement and OBR Economic and Fiscal Outlook now released online.

The OBR Economic outlook is interesting as it does not appear to include a new forecast for the critical RPI-X inflation figure, upon which fee increases will now be based.

That said, the new RPI and CPI inflation forecasts are, as expected, significantly higher than they were in March. This is due to Sterling depreciation primarily, and was cited by the Chancellor as a major reason for the lower growth forecasts for 2017 and 2018.

![screen-shot-2016-11-23-at-13-39-15]()

Rabbits and hats

It is worth noting, as the BBC’s Chris Cook has pointed out, the new £23 billion funds for capital investment returns spending in this area roughly back to 2010 levels.

And to conclude, perhaps we have the funnest announcement yet… we are abolishing the Autumn Statement, and the Spring Budget. But wait, we’re having an Autumn Budget and Spring Statement instead??? Apparently the latter will only respond to OBR forecasts, but include no fiscal changes “just for the sake of it”.

No change to departmental expenditure

There will be no change to departmental spending plans that were announced a year ago in the Spending Review. However, HE budget nerds will no doubt pore over the Department for Education’s budget to see that the entire HE budget from BIS into the new department.

This also means no end to protected spending areas: pensions, NHS, schools, and international aid. However, these will be reviewed looking forward to the next Parliament.

“World class tech corridor” and “Northern Powerhouse”

The new expressway between Oxford and Cambridge is confirmed, and is also couched in terms of supporting science and research “at our two best universities”. The new road will also link up Milton Keynes, home of the Open University.

In London, the adult skills budget will be devolved to the Mayor.

Yet Hammond is keen not to only focus on the South-East. The ‘Northern Powerhouse’ gets a mention, and the Chancellor announces the allocation of new money for regional growth and Local Enterprise Partnerships in the Midlands and the North. Some of this funding may find its way to universities and colleges, who work very closely with many LEPs.

Commitments to investment through borrowing

Hammond turns to the UK’s dire productivity gap: “it takes the average German worker four days, to produce what UK workers produce in five”. The turn is now very much to investment, funded through borrowing, to try to address this.

A big announcement: £23 billion in a National Productivity Investment fund. Is this all new money? Probably not, and it will include many of the announcements already made this week.

This includes the new rise in research and science funding, up to £2 billion by 2021, which is the first of these new investments to be confirmed by the Chancellor. This comes ahead of confirmations of new investment in housing and transport.

![screen-shot-2016-11-23-at-12-39-53]()

Headlines and forecasts

Hammond begins with the big macro-announcements, including the Office for Budget Responsibility’s growth and fiscal forecasts.

Growth will be lower in 2017 than was expected prior to the EU referendum, at only 1.4%. The OBR forecasts (with a great deal of hedging) that over the next 5 years, growth will be net 2.4% lower than it would otherwise have been due to “Brexit uncertainty”.

The old fiscal rules are now out of the window, and the government is no longer aiming to eliminate the deficit by the end of this Parliament. Instead, Hammond announces some new fiscal rules, which frankly, will give him plenty of wiggle room. Rules is perhaps a stretch; ‘fiscal guides’ seem more appropriate.

These new fiscal rulesare :

- Public finances “returned to balance” by end of the next Parliament.

- Borrowing under 2% by 2020.

- A new welfare cap to be overseen by the OBR

And we’re off

Philip Hammond is called to the dispatch box by John Bercow, and we begin.

A plant at PMQs

We have a question about the promised new £2 billion for research and science from Cheryl Gillan MP at Prime Minister’s Questions. The question is obviously a plant from the government to enable the Prime Minister to wax lyrical about this new spending, but it’s evidence that the government is clearly quite proud of itself for finding this extra cash and will make as much political and press capital out of it as they can.

Hopes, fears and expectations

We’ve been rounding up opinion from different parts of the sector about their hopes, fears and expectations for today’s Autumn Statement

Gordon McKenzie, Chief Executive, GuildHE:

I hope the Autumn Statement puts flesh on the bones of the industrial strategy and perhaps tells us something about what the government means by Brexit. I hope the Chancellor puts creating and exploiting knowledge at the centre of the industrial strategy and we see policies – and money – to support universities of all sizes and types to work with business to innovate, improve productivity and enrich people and places. I’d like explicit recognition and support for education as an industrial export sector.

But with lower growth and rising public sector debt the Chancellor doesn’t have much room for manoeuvre. So I fear further funding cuts and no clear sense of direction.

Julie Tam, Assistant Director of Policy at Universities UK:

Low inflation and strong employment figures in recent days will have been welcome news for the Chancellor. However, the impact of the Brexit vote is expected to be reflected in lower growth forecasts, and a weaker public finance position. We hope the Autumn Statement takes a long-term view and the government does not waver in its overall level of support for higher education and research, as committed to in the 2015 spending review. We do expect some changes in which department spends what, given the formation of the new BEIS and changes in responsibilities for the DfE.

We may hear more about the government’s plans for developing an industrial strategy, though it may be too early for related spending decisions at this stage. UUK’s submission to the Autumn Statement highlighted four main areas where government could maximise the contribution of universities in the industrial strategy. There is much potential for enhancing the roles of universities in supporting local growth and business through high-level skills, in tackling social mobility in disadvantaged areas, and to invest in research, innovation and infrastructure.

Professor Dave Phoenix, Chair of MillionPlus and Vice-Chancellor of London South Bank University:

The Autumn Statement provides an opportunity for the government to build on these strengths and provide the investment required to enable universities to play a full part in supporting the government’s ambitions post Brexit. The Chancellor should boost the capacity of all universities to trade in the global higher education market but also provide new funding streams to support the contribution that universities can make to the industrial strategy.

The Chancellor also has the opportunity to arrest the decline in the resources available to invest in the teaching infrastructure and provide new investment for the training and professional development of teachers and the health professions which universities help to deliver.

Sir Venki Ramakrishnan, President of the Royal Society:

I welcome the Prime Minister’s personal support for science. However, for our future prosperity and growth, it is both urgent and important to send a strong message that the UK will remain a leader in science and innovation, and a place in which to invest, work and seek collaborators. The UK is one of the best destinations in the world for research, nurturing talent from home and abroad, and one of the leading places to innovate.

Putting research and innovation at the heart of the Government’s industrial strategy will give it the best chance of success in ensuring broad economic prosperity through productivity gains. This will require a bold commitment to invest in research and innovation to build on our many strengths.

Gerard Dominguez Reig, Quantitative Analyst at the Education Policy Institute:

Theresa May has today pledged that £2bn extra a year will be made available to conduct research to boost innovation and productivity until 2020. The announcement aimed to reassure businesses and universities, two sectors that have been showing growing concerns over the effects of Brexit in terms of access to the common market and to European research funds, respectively.

The Autumn statement may clarify how much of the total sum will be made available to universities, either directly or through research councils, but it is unlikely that the awarding criteria will be set. In such case, the sector will be waiting for the criteria to be disclosed, as the priorities of the government may attempt to privilege some areas of research over others. If the governments’ criteria differ widely from those of the EU, then the expected resulting scenario is one with winners and losers and the sector facing further imbalances.

Previews on Wonkhe

On Monday we published two articles that looked ahead to today’s announcement.

A time for governing in prose (and spreadsheets) – Andy Westwood takes us on the walk down Hammond’s Passage. It’s dark, narrow and full political and economic dangers of all kinds.

Lessons from the front line of industrial strategy policy – Maddaliane Ansell of University Alliance used to lead the government’s industrial strategy work as a civil servant, and here she discusses what works and what to look out for as the new government tries to square a great many circles.

What we know so far

Good morning.

It’s not long now until the Chancellor will take to the dispatch box. As is common these days, a lot of the Autumn Statement’s content has been ‘trailed’ in the press in order to maximise news coverage. Two big announcements relate to higher education and universities in particular:

- On Monday it was revealed that £2 billion extra would be made available for science and research funding. As Jo Johnson pointed out yesterday at GuildHE conference, this is roughly a 20% real terms increase in the science and research budget, and will no doubt be welcomed by the sector. That said, we await the details on how exactly this will be broken down, and whether some of the new funding will take the form of tax exemptions and incentives rather than ‘hard cash’.

- This morning it was revealed that letting agent fees will be banned. This will no doubt please the National Union of Students, with many students in recent years campaigning on the topic of rent and cost of living. Banning such fees was an election campaign request from NUS, but the move will make little difference to costs in the non-private letting sector, and some have suggested it might actually lead to rent increases.

Welcome to the Autumn Statement Live Blog

We will commence the live blog later this morning.