There’s not generally a lot for higher education in the chancellor of the exchequer’s annual budget statement – but this year marks an exception.

We were expecting further details of two policies first announced earlier this year – a levy on international student fee income, and the promised return of maintenance grants for students from deprived backgrounds studying priority subjects.

Though the return of grants (even in a very limited form) was welcomed by students and the sector, the levy has been the focus of sustained lobbying from providers struggling to balance their books with the one area of income that has sustainably grown over recent years.

The budget also provides a few other unwelcome surprises – thresholds and interest rates have been frozen for plan 2 loan repayments (those made by the majority of recent graduates) until 2029-30, meaning that graduates will pay more. A tweak to pension salary sacrifices may make it even more expensive for some providers to employ staff. And the looming threat of a mammoth schools SEND debt being covered by departmental expenditure means that every area of education spending is likely to face pressure from 2027-28.

But it is the fee uplift for the next two years that is likely to get most attention.

Fee uplift

The higher rate for tuition fee loan caps will rise, as announced, in both of the next two academic years – to £9,790 a year in 2026-27 and up to £10,050 for 2027-28, with other statutory caps (including for classroom-based foundation years) rising in lockstep. These are expected to be the final two rises that apply to all providers – primary legislation will be laid that means future fee cap rises will be linked to the Office for Students’ revised teaching excellence framework.

It should also be noted that these are per year amounts, not the per credit amounts that the (as-yet unenacted) Lifelong Learning (Higher Education Fee Limits) Act allows the government to set – this is interesting as the entire funding system is due to move to a per credit basis (to allow for the Lifelong Learning Entitlement’s modular approach to study) from 2026.

While this decision has been widely trailed by the minister as evidence of her department addressing the financial problems faced by universities, it should be noted that both increases are (as usual) by OBR projections of interest rates which may differ from the actual interest rates. The rise of what is widely seen as the default tuition fee to north of £10,000 in 2027-28 is likely to trigger widespread commentary – if you believe the stories from the coalition years the original £9,000 figure was chosen precisely to avoid being above what was seen as a psychologically important £10,000 sticker price.

Here’s how that breaks down for all of the common fee caps:

| Fee caps | 2025-26 | 2026-27 | 2027-28 |

|---|---|---|---|

| With TEF and APP (FT) | £9,535 | £9,790 | £10,050 |

| With TEF and APP (PT) | £7,145 | £7,335 | £7,530 |

| With TEF and APP (Accel) | £11,440 | £11,750 | £12,060 |

| With APP only (FT) | £9,275 | £9,525 | £9,780 |

| With TEF only (FT | £6,355 | £6,525 | £6,695 |

| With neither TEF nor APP (FT) | £6,185 | £6,350 | £6,520 |

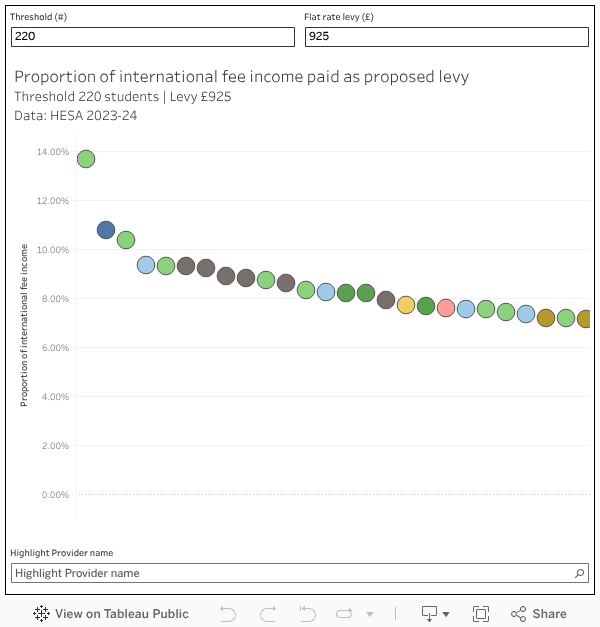

International student levy

We were expecting details of the international fee levy first announced in the immigration white paper – and these arrived via a consultation with a closing date of 18 February 2026.

The proposal is that from August 2028, the levy on international student fee income has been set at a flat rate of £925 per student (rising by inflation in following years), with the first 220 students entirely exempt. It is estimated that this will generate around £445m in 2028-29, equivalent to around 4.5 per cent of total international fee income across the sector. However DfE estimates that the sector would lose £270m for that year (equivalent to around 3 per cent of international fee income), suggesting that more than half of the cost of the levy would be passed on to students, given that the same estimates suggest 14,000 less students would come to the UK to study in that year.

Importantly, “international students” are defined as those who are registered for study during the year in question (excepting those who leave during the contractually protected first two weeks of study). Transnational provision, and provision at further education colleges below level 3, will not be in scope. And the system will be run by the Office for Students – there’s even an option to pay the levy quarterly by direct debit.

The impact analysis notes that the levy will – unsurprisingly – reduce the ability of the sector to cross subsidise domestic teaching or research from international fee, but we are reminded that this is before accounting for any reinvestment of the levy in the sector, and before accounting for the rise in domestic tuition fees (though as fee rises are linked, nominally at least, to inflation that last one is a little disingenuous.

The effect of a flat fee, as opposed to the blanket 6 per cent of international fee income levy first proposed in the annex to the immigration white paper, is to decrease the impact on providers who are able to charge higher fees per student. The “free” 220 students will keep many smaller specialist providers out of the levy entirely, meaning that proportionally more costs will fall on providers who attract large numbers of international students with lower fees.

While the University of Suffolk will lose nearly 14 per cent of international fee income to the levy(on 750 students) and the University of Huddersfield will lose 9.3 per cent, the University of Cambridge will lose just 2.69 per cent (on 7,315 students). The practical impact of the proposal will be that providers that are more likely to be drawing substantial parts of their operating income from international fees (and those more likely to be enrolling students with disadvantaged backgrounds) will be hit hardest. The charts in this article will help you compare this outcome with proportional models like the initial 6 per cent proposal.

We are not given a rationale for this change of approach, but it is fair to assume an active policy decision – to minimise the impact on those that make the most from international fees – based on soft power and international standing. It is a form of specialisation, perhaps.

Maintenance grants

Pretty much confirming that the policy on maintenance loans was back-of-a-fag-packet for Conference stuff, the documents collectively hide how much of the levy will be spent on the new maintenance grants. What we do know is that they’re coming in 2028-29, will be available to both new students and those already studying, and will be paid on top of maintenance loans.

The amounts will be means-tested – students from households earning at or below £25,000 will get the maximum (£1,000 in years one and two, £750 from year three onwards), tapering to £500/£375 for those with household incomes up to £30,000. The higher amounts in early years are designed to help with “access and initial progression”, but in reality it’s a cliff edge that hits students from care-experienced backgrounds particularly hard.

That doesn’t give us a total – grants will only be available for certain subjects aligned with the government’s economic priorities and Industrial Strategy. How many students there are left on a residual household income of 25k or less by 2018 is also not outlined. The eligible subject list hasn’t been confirmed – it’ll be informed by Skills England’s work on skills needs and may align with LLE priority funding categories. And students will need to be studying at least 120 credits per year (or full-time under current arrangements) to be eligible.

Maintenance loans

As (maximum) UG fees rise by projected inflation, so does maximum maintenance (and the PG loan schemes) by the OBR projection for Q1 2027 of 2.7 per cent. Of course the OBR has been wrong before, and may be wrong again – this year’s 3.1 per cent increase (based on Q1 2026) now shows up as 4.1 per cent in revised OBR forecasts, an error that nobody goes on to fix and so compounds in its impact over time.

In addition, there’s no sign of that parental (residual household) income threshold for parents chipping in changing either – and now that the minimum wage is firmly over £25,000, will almost certainly mean a collapse off a cliff in the number of students able to access the maximum. This year DfE’s own estimates reckon that a maximum loan increase of 3.1 per cent will only result in an average loan increase of 2.6 per cent – expect (much) more of that by the end of the Parliament.

While we’re on parental contributions, buried in the documents is another nasty sting. Right now, if you have two kids at university at the same time, the system recognises that your money has to stretch, and works out a “parental contribution” based on your household income, then splits that between the two students. So if the calculation says “this family can afford to put in £2,000”, and you have two undergrads, the system assumes roughly £1,000 per child – and each student’s maintenance loan is a bit higher to reflect that you are not magically doubling your contribution.

It turns out that the LLE change will mean the SLC stops doing that split for people on the new LLE-style maintenance – each young person’s maintenance will be worked out on the household income as if they were the only one studying. So using the same example, the system would effectively assume you can contribute £2,000 to Child A and £2,000 to Child B. It’s “simpler” because in a modular, on-off, part-time LLE world the SLC will no longer have to track who else in the family is studying and constantly recalculate the split.

But for a “traditional” family with two young full-time undergrads at the same time, it quietly removes a small protection you currently get when more than one child is in higher education.

Plan 2 threshold freeze

You might remember, back in the Summer of 2023, when Bridget Phillipson was touring the studios to declare that graduates will pay less under a Labour government:

Reworking the present system gives scope for a month-on-month tax cut for graduates, putting money back in people’s pockets when they most need it. For young graduates this will give them breathing space at the start of their working lives and as they bring up families. This is a choice that the Tories could be making now to deliver a better, fairer system for our graduates and for our universities…. Labour will not be increasing government spending on this.

There was never a detailed explanation of how that magic trick would be pulled off – although it was likely to have been based on London Economics’ stepped repayment modelling, which depended in part on the reintroduction of real interest rates post-graduation (between 0 per cent and 2 per cent) for graduates with earnings between £27,571 and £57,570.

Either way – at least for Plan 2 borrowers – the budget very much breaks that pledge. For anyone who started a degree between 2012 and 2022, the repayment threshold will be frozen at £29,385 in cash terms for three years from April 2027. Instead of that threshold rising with prices or earnings, it just sits there while wages (hopefully) go up – which means more graduates crossing the line into repayment sooner, and those already repaying handing over a bigger slice of their real income than they would have done otherwise.

It’s very much a stealth extra tax on graduates layered on top of already frozen income tax and National Insurance thresholds, and it shifts (even) more of the cost of the system away from the state and onto a cohort who have already endured one round of threshold suppression under Michelle Donelan’s “fairer sharing of the burden” reforms, have watched the “deal” they signed up to being repeatedly tweaked after the fact, and had been led to expect a “month-on-month tax cut” rather than another quiet squeeze.

The Treasury’s justification consciously echoes Donelan’s line about graduate earnings premiums and fairness to non-graduates, but in practice this looks less like a principled reset of student finance and more like a return to the same playbook – using Plan 2 borrowers as a handy, captive tax base until the reality shows up on their payslips. For Reeves, it generates £285m in 2025-26, a big £5,915m “gain” in 2026-27 (that’s mainly the accounting revaluation of the loan book, not cash), then £255m in 2027-28, £290m in 2028-29, £355m in 2029-30 and £380m in 2030-31.

Wider measures for students

Rising National Living Wage and youth rates mean a substantial chunk of full-time students working in hospitality, retail and care will see higher hourly pay, although given the volume of jobs lost in these sectors in recent years (with similar warnings from those industries overnight), they’ll need to find a job first.

The creation of a “Fair Work Agency” with explicit focus on enforcement in “high-risk” sectors is also, if successful, is likely to impact on international student incomes in a way that few like to talk about, but pretty much everybody knows (working more than 20 hours a week, cash in hand, with no rights).

Extending the £3 bus fare cap will help, holding prescription charges steady all keep day-to-day pressure in shared student houses and commuter budgets a little lower than it would otherwise be, and taking around £150 off the average energy bill by shifting decarbonisation costs off bills and onto general spending won’t matter much given “all-inclusive” bills in halls and HMOs.

Free emergency contraception in pharmacies closes an obvious gap in sexual health provision for a very student-heavy age group, while the cap on ticket resale prices cuts straight across the live events market some students use.

Add all the measures up, and you might expect student poverty to show up in the annual release of the distributional impact on households analysis that gets produced to accompany budget day – but alas it remains the case that tuition fee loans show up as household income in the DWP’s Households below average income (HBAI) statistics, which means that the increase in maximum fees will see an HMO with 5 students in it looking 50k better off than they really are.

Other bits

The chancellor capped national insurance contribution exemptions for salary sacrifice into pensions at £2,000 – employees who pay more than this amount each year into pensions will need to account for employer national insurance contributions on additional amounts. A note from sector employers association UCEA before the budget reminded the Treasury that this approach is widely used by universities, and calculated that a cap could cost individual USS institutions an additional £1-3m each year with a total cost to the sector north of £50m – and there are going to be impacts relating to other pension schemes too.

One of the biggest current issues with the wider education budget, and one that has pushed many local councils towards bankruptcy, is the rapidly rising cost of school provision and other support for pupils with special educational needs (SEND). Currently the costs of this provision are nominally covered by local councils, but are subject to a statutory override which means that the sums involved are not included within council deficit calculations. The budget confirms the June announcement that this arrangement will end from 2027-28, with costs (due to hit around £5bn) covered from that point within departmental expenditure limits.

This has a clear impact on other areas of government spending, and if the Department for Education is to be made responsible it is likely that at least some of this funding will have to be found via cuts to other budgets, including for tertiary education.