Every July, the Department for Education publishes its student loan forecasts.

It’s the department’s annual best guess at what students will borrow, what graduates will repay, and how much of the difference the taxpayer will swallow.

This year’s edition manages a trick that ought to be impossible. Graduates are going to pay more than the government thought last year – hundreds of millions of pounds more, every year, thanks to the repayment threshold freeze announced at Autumn Budget 2025.

And the system is going to cost the government more anyway.

Both things are true at the same time, and understanding why tells us most of what we need to know about where England’s (and then by proxy devolved nations’) student finance system is heading.

Pay more

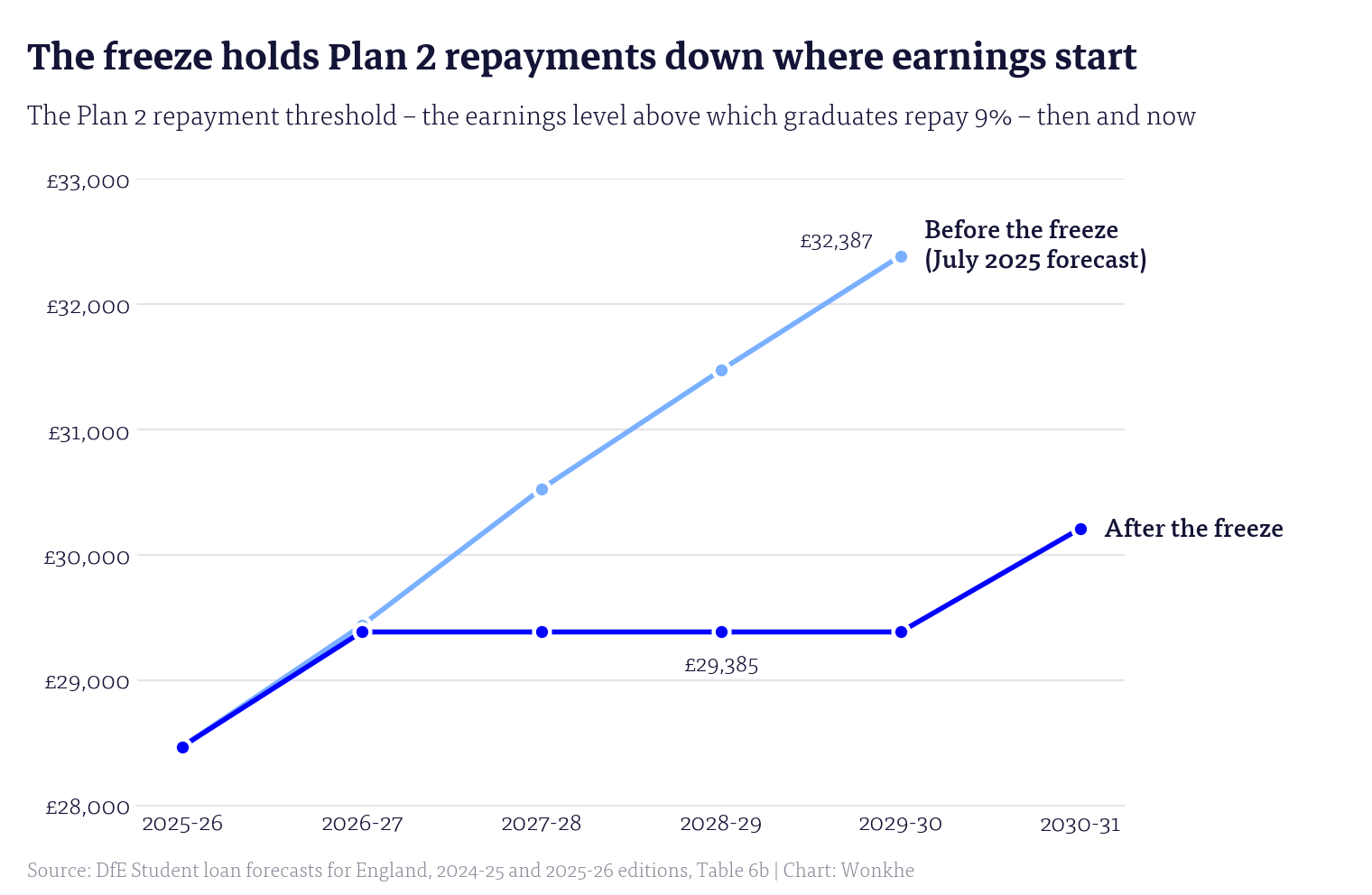

Let’s begin with the cash. If you’re on Plan 2 – broadly, anyone who started an undergraduate course between 2012 and 2022 – you repay nine per cent of whatever you earn above a threshold.

That threshold is now frozen at £29,385 until April 2030. Last year’s forecast had it rising with inflation to about £32,400 by the end of the decade.

The freeze means an extra £3,000 slice of everyone’s salary now has nine per cent skimmed off it – not because anyone is earning more, but because the line moved.

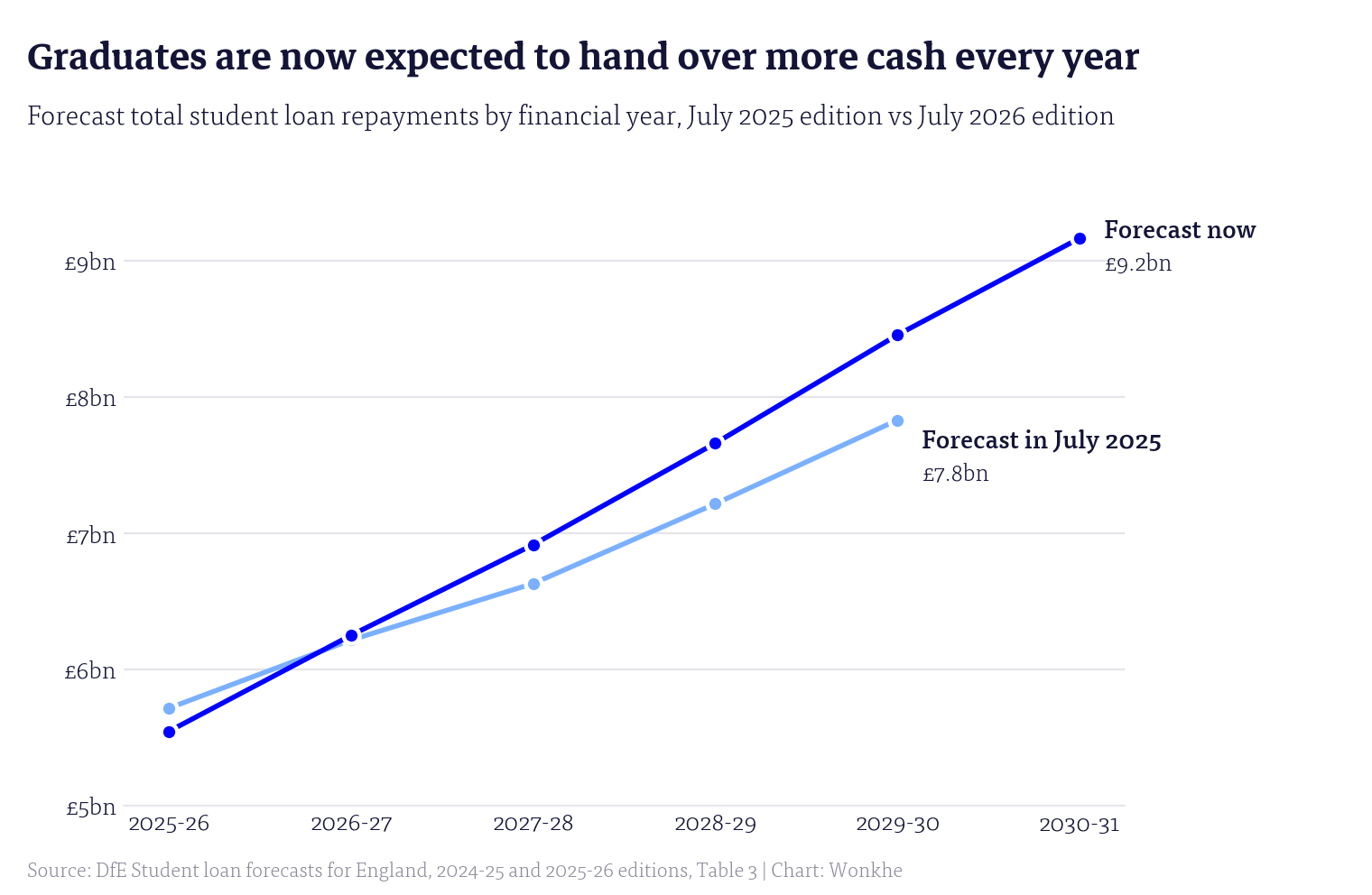

For an individual graduate earning above both lines, that’s roughly £103 extra in 2027-28, £188 in 2028-29 and £270 in 2029-30 – call it £565 over three years that last summer’s forecast didn’t ask for. In aggregate, repayments in 2027-28 are now expected to be £6.9 billion, up from £6.6 billion in last year’s edition – by 2029-30 it’s £8.5 billion against £7.8 billion.

And dividing the Plan 2 repayment total by the number of borrowers earning above the threshold gives you the trajectory for the typical repayer – £1,464 this year, £1,885 by 2029-30, £2,010 by 2030-31 – 29 per cent more cash within five years, far ahead of anything the forecast assumes about pay rises.

When the government moves the goalposts on five and a half million Plan 2 higher education borrowers at once, the money shows up fast.

Lose more

So with graduates paying more, the government’s losses on the loan book should be shrinking. But they are not.

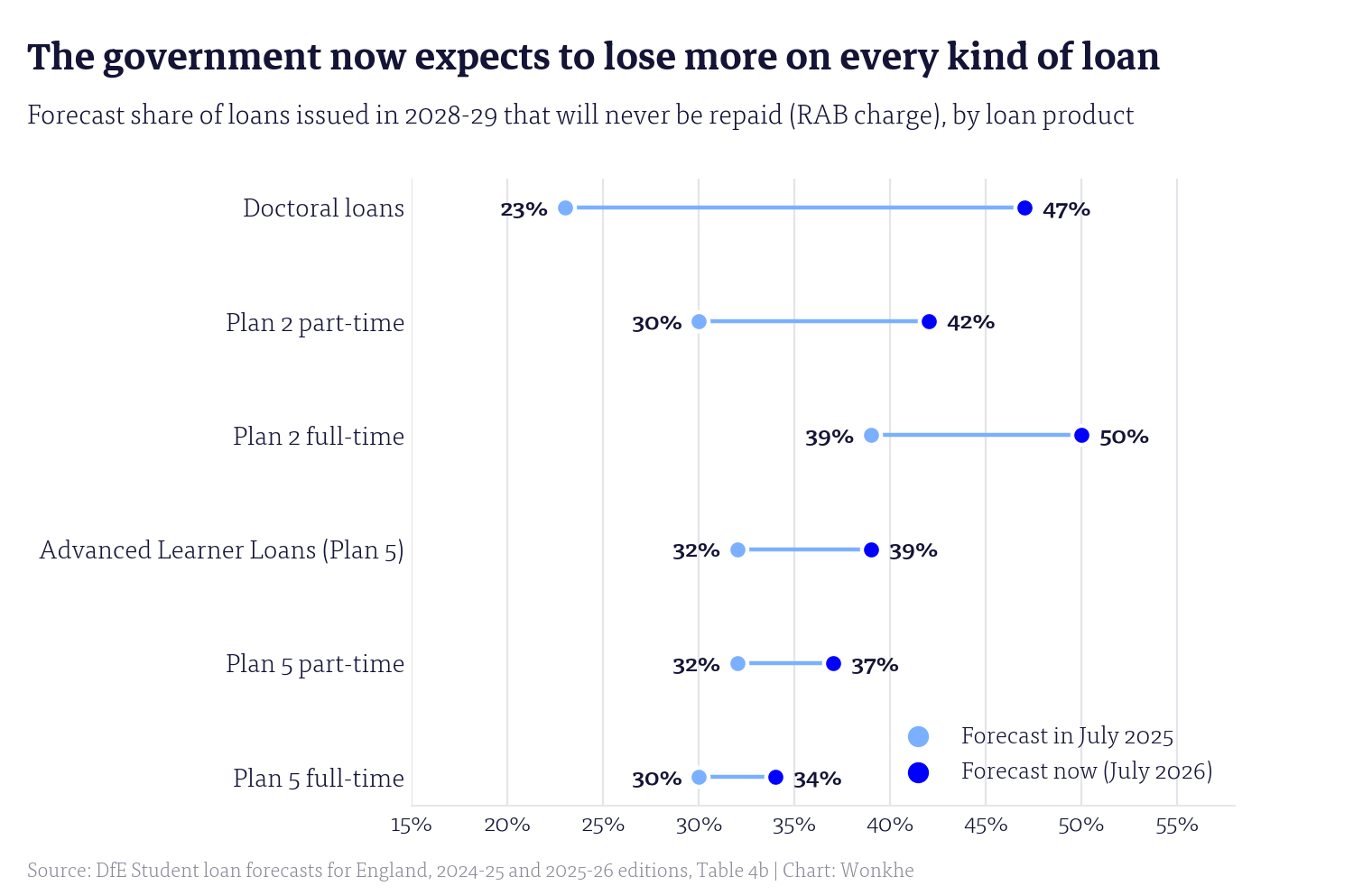

The key number here is something called the RAB charge. Strip away the acronym and it answers a simple question – of every pound the government lends to students this year, how much does it expect never to see again?

Most graduates don’t repay in full – the debt is written off after 30 or 40 years – so some fraction of each year’s lending is really a grant in disguise, and the RAB charge is the government’s own estimate of that fraction.

That fraction just jumped, on every single loan product. On Plan 2 full-time loans it’s 39 per cent, when last year’s edition forecast 34 per cent for the same year.

On the newer Plan 5 loans – everyone who started from autumn 2023 – it’s 33 per cent against a forecast 30.

Plan 5 part-time is up six points, as are Advanced Learner Loans on Plan 5 terms. The RAB charge on doctoral loans has more than doubled, from 23 per cent to 47 per cent.

And comparing like with like on the same future year, the deterioration compounds – for loans to be issued in 2028-29, last year’s edition said 39p in the pound would be lost on Plan 2 full-time. This year’s says 50p.

No, it’s not just the accounting

The usual caveat at this point involves something called the discount rate, so strap in. A pound repaid in 2050 is worth less to the Treasury than a pound repaid today – so when the government adds up what a loan is worth, it shrinks all those future repayments into today’s money using an interest rate it sets itself.

Nudge that rate up and future repayments look smaller, the loan book looks less valuable, and the RAB charge rises – without a single graduate’s circumstances changing. The Treasury has changed this rate in every one of the last six editions of these forecasts, which is why seasoned readers reach for the salt whenever the RAB moves.

Not this time. DfE’s own sensitivity tables – the “what if” workings published alongside the forecasts – suggest this year’s discount rate change explains only around a point and a half of the five-point rise on Plan 2. And there’s a second measure that settles it.

Since the Office for National Statistics reformed loan accounting in 2018, every pound lent to students is split at the moment it’s issued into two jars – the part the government expects to get back, which counts as a loan, and the part it doesn’t, which counts as public spending and hits the deficit there and then.

The size of that second jar – the “transfer proportion” – is worked out using the interest rates charged to borrowers themselves, not the Treasury’s own adjustable rate. It is, by design, the measure the Treasury can’t fiddle.

And it rose too. On Plan 5 full-time loans, 34p in every pound lent this year goes straight into the spending jar, against 31p forecast last year. On Master’s loans, 18p against 10p. By 2028-29, 66p of every pound lent to a Plan 2 full-time borrower is expected to be spending rather than lending – last year the forecast said 61p.

When the tamper-proof measure and the adjustable measure move the same way, the story isn’t accounting. The model has just marked down what graduates are going to earn. This year’s forecasts absorb three more years of real earnings records – the tax data underpinning the model now runs to 2024 – and what actually landed in graduates’ pay packets was worse than what the model had been assuming.

On DfE’s own workings, the threshold freeze should have improved the Plan 2 position by something like six points by the end of the decade. Instead it worsened by eleven. The Treasury reached for the same lever it always reaches for – and the lever isn’t big enough any more.

Fewer students, too

Buried further down is a restatement that would be the lead in any other year. Last July, DfE expected 541,000 undergraduate entrants to take out loans in 2024/25 – an academic year that was all but finished when the forecast was published. The new edition puts that year at 485,000.

Fifty-six thousand entrants, more than ten per cent of the intake, evaporated between two editions of the same statistical series – on a year that was already over.

So where did they go? One tempting theory – that better-off families have started paying upfront and skipping loans altogether – doesn’t survive contact with the data. The release’s own household income table shows borrowers from households on £65,000 or more rose 13 per cent in the latest year available, and the group who don’t bother applying for means-tested support (disproportionately the comfortable) is flat at 22 per cent.

Nor is it a collapse in students overall – the Student Loans Company’s outturn figures show the number of full-time tuition fee loans actually paid in 2024/25 went up half a per cent – the first rise since 2021/22. The stock of students grew – it’s specifically new entrants that came in far below what DfE expected – and within that, part-time entrants were restated down 18 per cent.

Two things fit that pattern. First, the old forecasting model was simply wrong – built without enrolment outturn data during the Data Futures debacle, extrapolating pandemic-era application growth that never materialised. Some of those 56,000 entrants were never real.

DfE has responded by scrapping the model entirely, replacing it with projections built directly on SLC payment records – and the table showing how well the old model had been performing has quietly disappeared from the methodology.

Second, the Department’s own crackdown on franchised provision – degrees delivered by subcontracted providers, where DfE has been chasing “fraud, abuse of public money and poor value for students” – landed on exactly the segment that had been driving entrant growth, complete with payment suspensions and the reclassification of weekend courses that cut maintenance eligibility for some 22,000 students.

Frustratingly, since November 2025 the SLC “is no longer able to calculate or publish” take-up rates – the proportion of eligible students who actually take out loans – another casualty of Data Futures. At precisely the moment the sector needs to know whether debt-averse students are abandoning the system, the official statistic that would tell us has ceased to exist.

The franchising bill lands on everyone

For the first time, franchised provision is modelled explicitly – but only on the way in.

The forecast now projects franchised and directly-delivered entrants separately, and applies a “franchising adjustment” simulating the Department’s enforcement – some franchise operations keep growing, some hold steady, some shrink, some stop recruiting, removing an estimated 6,400 entrants in 2026/27 alone – with DfE noting, in a loan forecast methodology of all places, that some displaced students “may choose not to enter HE”.

The adjustment doesn’t yet include the new requirement for larger franchised providers to register with the regulator, so there is more downside already signposted for next year.

But on the way out – repayments – franchised students don’t exist. They’re registered with their lead providers, so in the earnings model they’re indistinguishable from everyone else there. No RAB charge is published by provision type, and no repayment forecast separates them.

Which means that as the model absorbs the actual earnings of the cohorts recruited during the franchise boom – and those are exactly the years the new tax data covers – any poor outcomes show up not as the attributable cost of a policy failure but as “graduates are earning less than we thought”, raising the RAB charge on everyone’s loans.

DfE now forecasts franchised entrants separately, so it could forecast franchised repayments separately. Until it publishes the cost of the loan book by provision type, there is no way to know how much of this year’s across-the-board deterioration is the franchising experiment coming home to roost – and every graduate, and every taxpayer, is carrying an unitemised share of the bill.

Getting less

Meanwhile, what does the borrower get for all this? Less, on every line you can measure.

The maximum maintenance loan is uprated with inflation each year – but the median maintenance loan actually paid is forecast to grow at just 1.2 per cent a year over the forecast period, against fee loans at 2.7 per cent, and it actually falls in cash between 2026/27 and 2027/28.

By 2030/31 that’s roughly a seven per cent real-terms cut in the typical student’s living-cost support. It’s already happening – SLC’s outturn shows the average maintenance payment fell 3.6 per cent in cash last year.

The likely mechanism is familiar – the household income thresholds that determine maintenance entitlement have been frozen in cash for years (£25,000 for full support, unchanged since 2008), so every year of wage inflation drags more families into partial entitlement while the headline maximum rises. The maximum is a shop window – the median is what students live on, and the gap between them widens every year of this forecast.

Odder still is that the maintenance grants the government announced at the same Budget as the threshold freeze – up to £1,000 for low-income students from 2028/29 – appear nowhere in this forecast.

The document says it incorporates “existing government policy announced by April 2026” – the grants were announced in November 2025, and the skills minister told the Treasury Committee this month that grant-eligible students may choose to take out smaller loans as a result.

Unlike the Lifelong Learning Entitlement – absent for the fifth edition running, two months before applications open, with the exclusion at least declared – the grants seem to be missing silently. A six-year forecast now spans the start dates of two announced policies it doesn’t contain.

Who carries it

The distributional tables – expanded this year, to DfE’s credit, with new breakdowns by sex and age – show who is carrying the repricing.

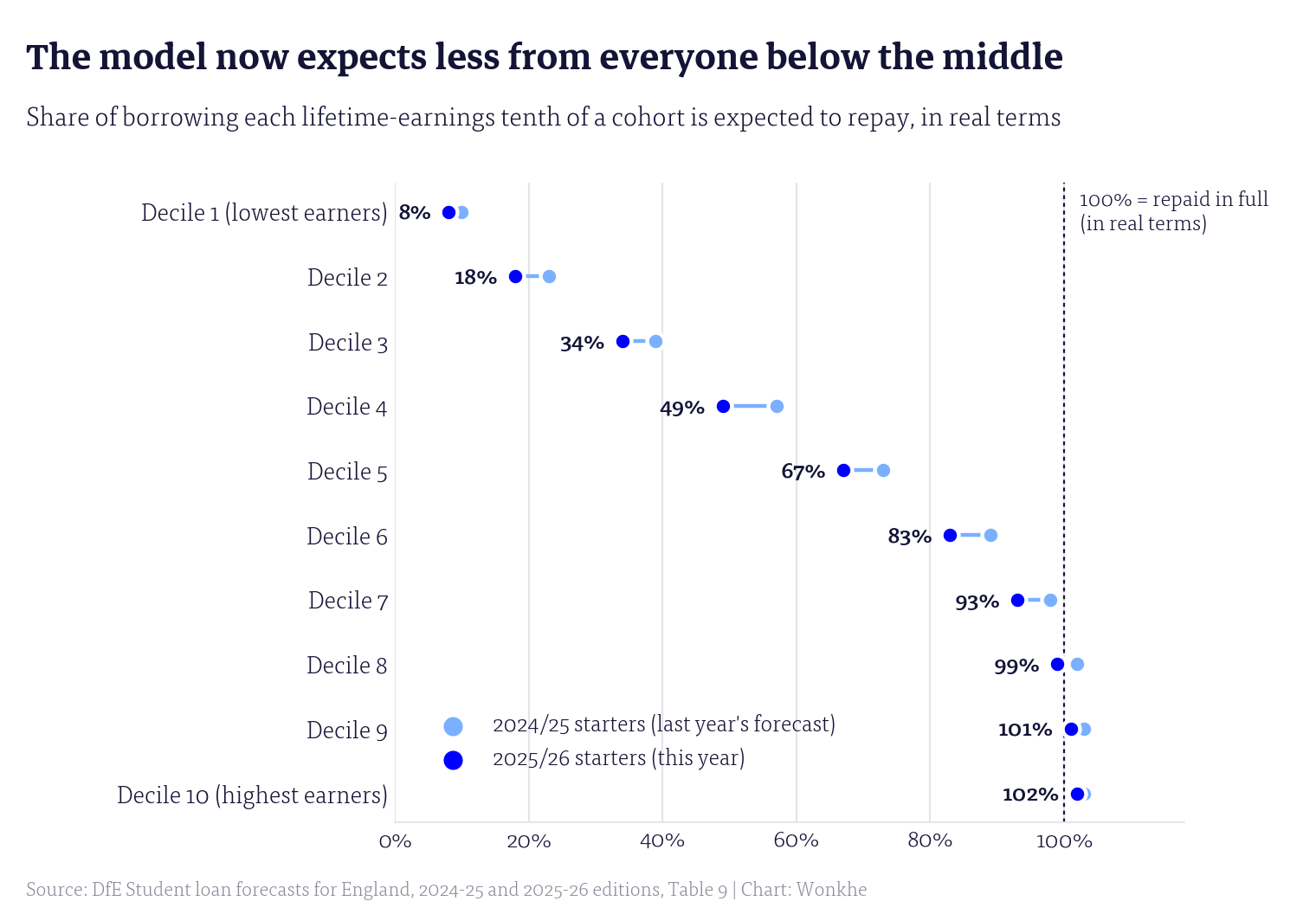

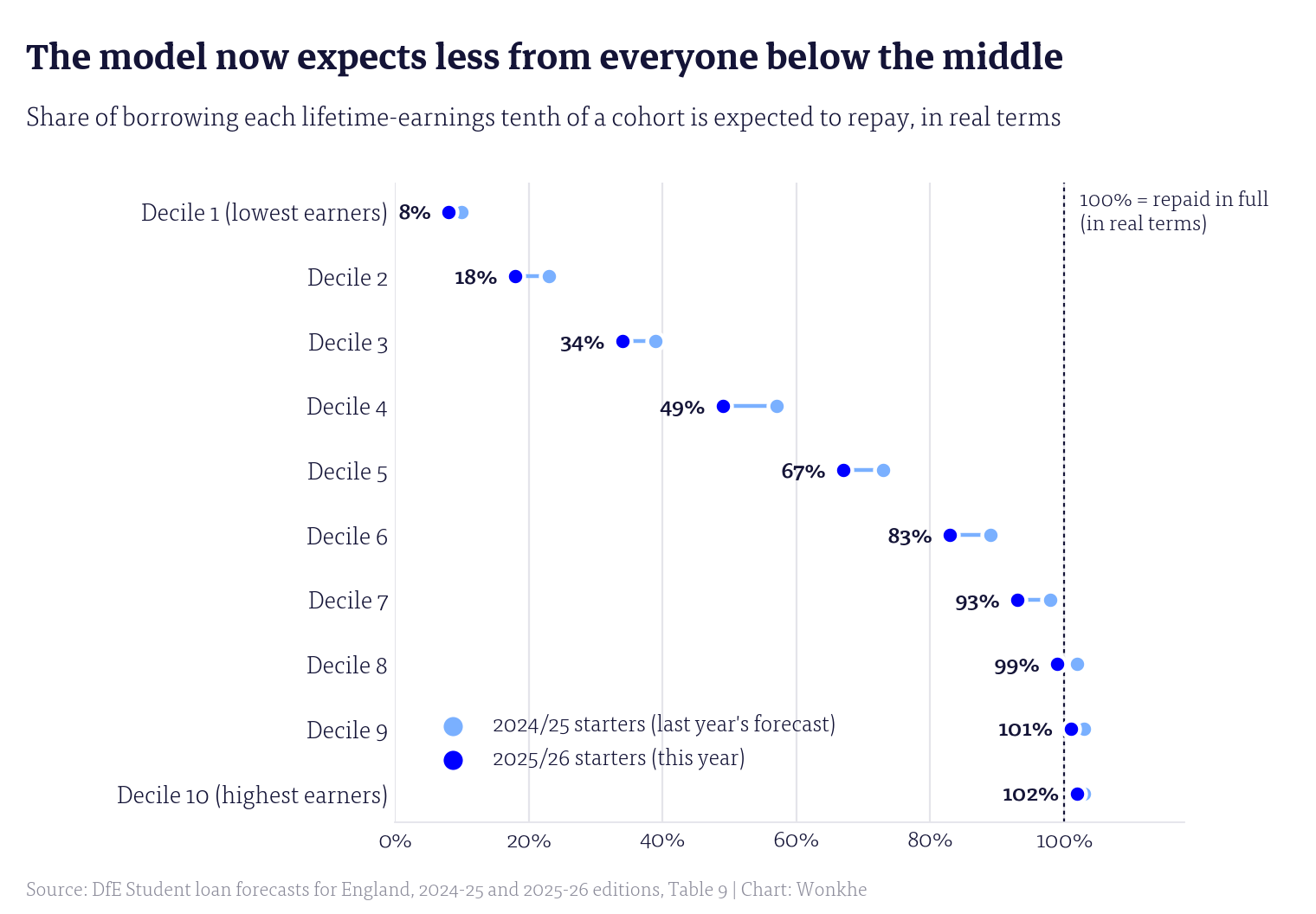

DfE sorts each year’s borrowers into ten equal groups by what they’ll earn over their working lives, and forecasts how much of their borrowing each group will repay. The bottom tenth of this year’s intake is now expected to repay £3,300 – eight per cent of what they borrowed – down from £3,900 and ten per cent for last year’s.

And the typical borrower in every one of the bottom five groups now reaches the 40-year write-off point still owing money.

Women repay £2,200 less than men on average, and the typical woman takes five years longer to finish – a gap DfE has now published, and explained as reflecting “generally higher lifetime earnings among males than females”, in plain terms for the first time.

Borrowers starting repayment at 41 or older are expected to repay 35 per cent of what they borrowed, with the methodology newly candid that the most common way this group’s loans end is not the 40-year write-off but death.

Meanwhile the proportion of new full-time borrowers expected to repay in full ticks down from 56 to 55 per cent – these are Plan 5 borrowers, and curiously the median one is now expected to clear their loan in 30 years rather than the 31 forecast for last year’s cohort, even as the model marks their earnings down.

And the headline statistics tile has dropped the footnote pointing at last year’s embarrassing revision, when 65 per cent became 56 after DfE noticed it had been counting cohorts of students who hadn’t started yet.

The system is being repriced in real time

Put the pieces together and this edition reads like a system having its price re-marked, all at once. Fewer entrants than forecast, less lending than forecast – around £1.7 billion a year lower by the end of the decade – and worse graduate earnings than forecast.

A first wave of 2.18 million Plan 5 borrowers hitting their repayment start dates by 2030-31 – fewer than half of them expected to earn enough to repay a penny that year. Interest accruing on the book at £15.5 billion a year by the end of the forecast against £9.2 billion coming in – and in the long-term projections, annual repayments don’t exceed annual new lending until 2071-72.

And remember what even these numbers don’t show. Every pound of the £21 billion lent this year is borrowed by the government up front, in cash, on gilt markets where the cost of borrowing has shot up – interest the Treasury pays for decades while it waits for repayments that peak in the 2070s, and which appears in none of the measures above.

Stare at the accounting long enough and the incentives it hands the Treasury become uncomfortably clear. A system where the state loses forty-odd pence in the pound on each new student makes fewer students a saving – and makes the “most expensive” students the ones forecast to earn least, which in practice means mature students, part-timers and those arriving without traditional qualifications – precisely why the government would rather they do a module they’ll pay back the fees on in full.

And the ratchet only turns one way. Make the terms kinder – raise a threshold, cut the interest – and the expected write-offs across the entire historic loan book crystallise as a single eye-watering year of spending – make them harsher and those same historic write-offs shrink, booking an instant one-year windfall, which is how a £5.6 billion “saving” appeared the moment the freeze was legislated.

As John Blake observed for the Post-18 Project this week, no chancellor faced with that asymmetry will ever choose generosity – the accounting punishes it upfront and rewards meanness immediately, whatever either choice does to students, graduates or the public finances over the forty years that actually matter.

The one lever that reliably improves the headline numbers – making graduates pay more – has been pulled again, and the deterioration underneath is visible, on every measure at once, including the one designed to be tamper-proof.

Students are borrowing more for maintenance that buys less, graduates are repaying more for a system that writes off more because they’re worse off than predicted, and everyone is miserable about a loan system which commands the confidence of nobody.

The walls, you might say, are no longer closing in. They already have done.