The appointment of John Blake as the Office for Students’ Director for Fair Access and Participation coincided with quite a period for the UK economy.

On the day his appointment was announced in November 2021, CPI inflation was up at 4.6 per cent – and then continued to climb, up to a high of 9.6 per cent 11 months later.

We know, by now, that the Department for Education’s increases to maximum maintenance loans have failed to match actual inflation for a few years now.

We also know that the continued failure to uprate the threshold over which we expect parents to chip in – stuck at £25,000 since 2007 – also means that the income available to home domiciled students has been further squeezed.

In that mix are bursaries and scholarships. Ever since the creation of the Office for Fair Access back in 2004, the amount of additional student financial support doled out by universities has represented a classic postcode lottery – and while “give students more money” has gone out of fashion as a simplistic answer to access and participation, they have continued to play an important role.

In his big speech to the Universities UK Access Participation and Student Success conference, Blake said that here is “no point pretending” that diminishing financial resources and expanding equality needs are not in tension.

He also said that balancing those imperatives will require “agility and good sense” from those it regulates, and will require it from OfS as the regulator.

The question on my mind ever since John Blake’s appointment – and his new regime of access and participation planning – has long been what might come of additional student financial support in a context of rapidly rising (and now falling) inflation for both students and their providers.

And as the tension between student resources and provider resources gets tighter, we’re now starting to get some clues.

Approved plans are emerging

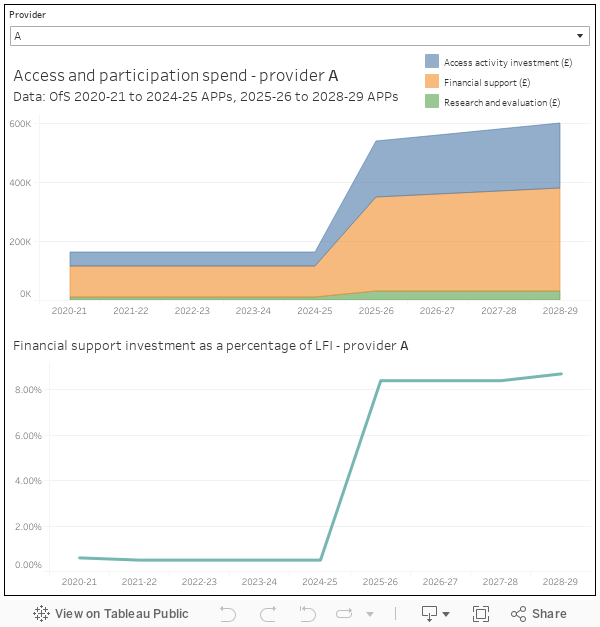

In scope here are the fourteen providers whose Access and Participation Plans for 2025-26 to 2028-29 have now been published on the Office for Students’ website. I’ve not included those who took part in last year’s pilot exercise, and I’ve anonymised them. There’s a good range of provider types and sizes in there, although notably none from the Russell Group.

What’s represented above are the planned investment figures for each of the three types of APP spend – access activity investment, financial support and research and evaluation – lifted from two sources; the 2020-21 to 2024-25 APP, and the newly approved 2025-26 to 2028-29 APP.

There are a lot of caveats on drawing conclusions. Both are figures in plans, not actuals. Neither set of figures tells us about spend per head helped, or spend per student in general. Neither tell us about whether the provider has contracted or expanded, and if so whether that contraction or expansion has been bigger or smaller in APP target groups.

But it does give us clues – lines of enquiry if you will – on what’s set to happen to bursaries, scholarships and hardship funds. If nothing else, on this sample at least, the total planned student financial support in 2020-21 for this group was £20m, but will have fallen to £17m by 2028-29. Really?

The sharp drops between plans do at least give us things to look for in the narrative of the published plans.

Smoothing and sharpening

One university is ending its core bursary scheme at the end of 2026, intending to “reposition” support to the success and progression stages of the student lifecycle, partly by aiming to create more opportunities for flexible paid work on campus. It doesn’t say how many jobs it will create, nor how it intends to target those jobs at those who need the money. More notably, while there’s evidence to support spend on its target areas, it doesn’t evaluate any negative effects on its current performance via the removal of up to £1,000 for first year UGs whose household income was £25,000 or under.

A small and specialist provider, on the other hand, is broadening who gets a bursary and how much they get. It says that it does not currently collect applicant or student household income data, and holds no data on Free School Meals – a revelation which seems bold to include – but given its undergraduate programs demand high engagement (limiting students’ ability to pursue paid part-time work) and rising applications for hardship funds it seems to be tripling who will will get one.

Another provider is raising its core bursary for the lowest-income from a maximum of £1,300 to £1,600 (2025–26), and increasing its targeted bursary for care leavers and estranged students from £2,500 to £3,000 annually. The new plan introduces more financial literacy guidance for eligible students.

It knows that ongoing cost pressures affect students’ abilities to engage fully with university life – especially those from low-income backgrounds, mature students, and other groups with limited financial support – and feedback also indicated that many are increasingly reliant on part-time work which then impacts their academic performance and well-being. But these seem to be qualitative observations.

One university adopts what we might call a smoothing approach. The last plan offered higher initial support but reduced the bursary in subsequent years – families on up to £25,000 got £2,000 in year one, and £1,100 in other years. That’s now set to be a flat £1,000 for families on up to £35,000 – with more assistance available for care leavers and refugees. Unless I’ve missed it, the new plan doesn’t evaluate the potential downsides of reducing first-year support on retention, engagement, or reduced financial strain.

Another is moving from a straightforward bursary of £1,000 for households under £15,000 to a maximum of £1,500, tapering down towards £35,000. That might reflect how few students ended up entitled to its old bursary rather than particular generosity – the planned financial support will shift from 10 per cent of increased fee income in 2020-21 to 8.2 per cent by 2028-29.

We might have expected inflation to be mentioned in the published plans – either in the analysis of extra costs that those on low-incomes might be facing, or in commitments to increase any financial requirements between now and 2028. Astonishingly, while “increased cost of living” is often asserted, across all twelve inflation is only mentioned in relation to the maximum tuition fee that providers are hoping to charge – never in relation to the costs that students might face. It tends to be mentioned as a qualitative contextual rather than quantified in any way.

More to come

We only, so far, have twelve to look at – and I’m conscious that the above doesn’t take into account the risks that those providers have selected, the performance data on outcomes they were each looking at, or the broader way in which OfS evaluates the “credibility” of each of the plans.

But so far, there’s little evidence that planned reductions in student financial support have been evaluated for negative impacts, little evidence that providers have been quantifying the impacts of real-terms cuts to maintenance support, and little evidence that providers have been quantifying the impacts of inflation on their students’ costs.

I know that providers are trying to more with less – but given the numbers and warnings that providers themselves have been putting on their own costs, their own funding and their own future provision, this is already starting to feel like a system that is fatally unaware of the wider financial context in which students attempt to access and participate in higher education.