It’s impossible for a government to talk about industrial strategy in the UK without mentioning British Leyland, the auto conglomerate effectively nationalised after going bankrupt in 1975, and which finally expired in 2007.

The story of British Leyland is often used to illustrate the folly of governments ‘picking winners’, which inevitably produces outcomes like cars with square steering wheels. So it’s not surprising that the government’s latest Green Paper, Building our Industrial Strategy, begins with a disclaimer: this isn’t a 1970’s industrial strategy, but a new vision, a modern industrial strategy that doesn’t repeat the mistakes of the past.

As pointed out last week by the Business, Energy, and Industrial Strategy Select Committee, this document isn’t actually a strategy yet, and it’s a stretch to describe much of it as new. But it is welcome, nonetheless. Above all, the document focuses on the UK’s lamentable recent productivity performance, and the huge disparities between the performances of the UK’s different regional economies. It puts science and innovation as the first “pillar” of the strategy, and doesn’t pull punches about the current low levels of both government and private sector support for research.

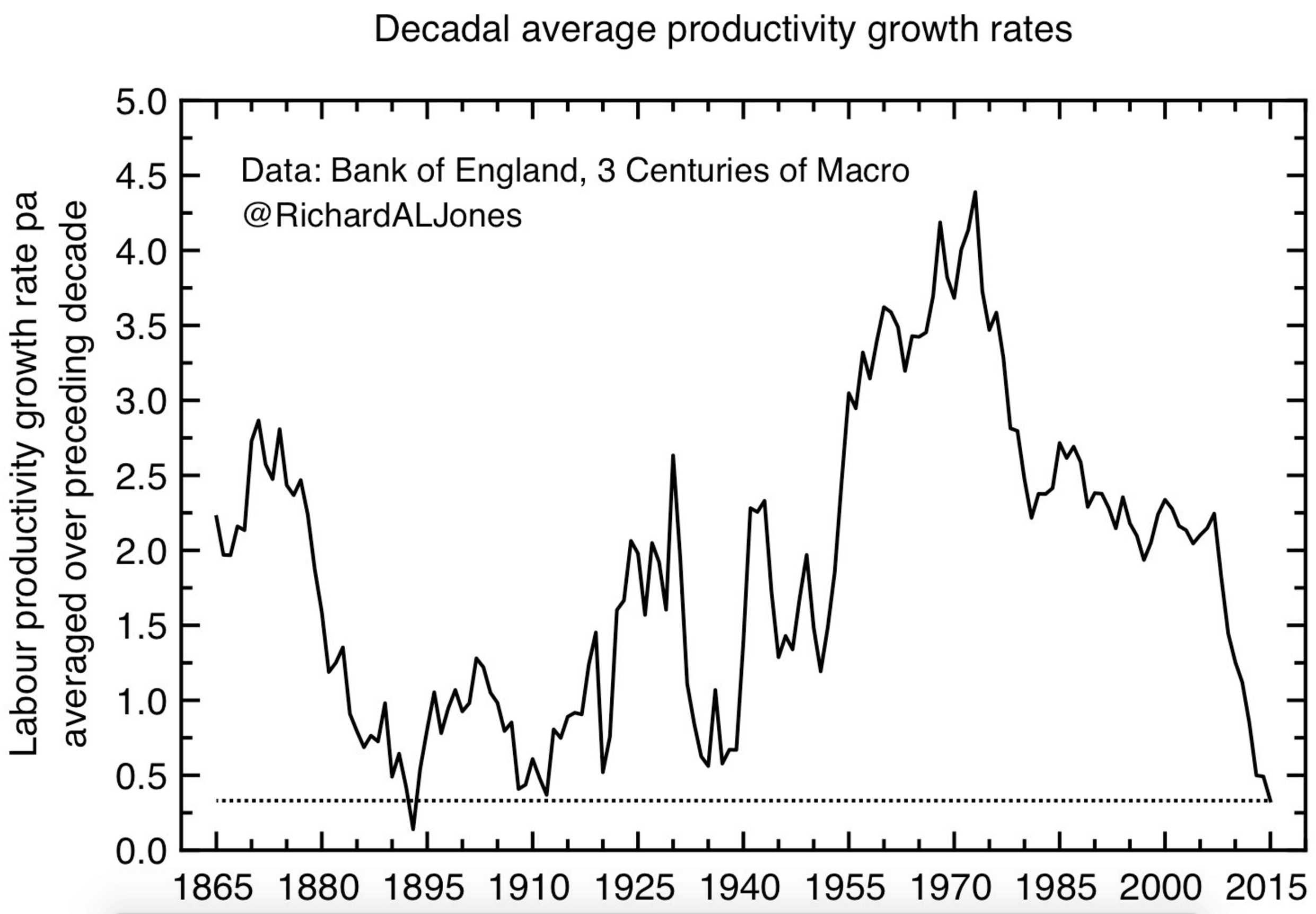

UK Productivity has grown less over the last ten years than over any previous decade since the late 19th century. Decadal average labour productivity growth, data from Thomas, R and Dimsdale, N (2016) “Three Centuries of Data – Version 2.3”, Bank of England

Industrial strategy over the decades

It is important to look at what’s proposed today in the light of what’s gone before. Although the words “industrial strategy” come in and out of fashion, and we’ve seen productivity plans, industrial policies and innovation frameworks, the conceptual underpinnings have remained remarkably stable, with a strong emphasis on the idea of correcting market failure.

Going back to the beginning of this parliament, we had the ‘productivity plan‘ in July 2015, in which long term investment in science and innovation, skills and infrastructure would lead to a dynamic economy.

In the days of the Coalition, we had “a long-term, whole of government approach to support economic growth”, focused on skills, technologies, finance, government procurement, and sector support. A credit card sized explainer from 2013 gave a handy reminder of the eight great technologies and eleven key sectors that would be focused upon. The Coalition’s approach was in many ways a continuation of that begun by Peter Mandelson, whose April 2009 document, New Industry, New Jobs, marked his post-financial crash conversion to interventionist government.

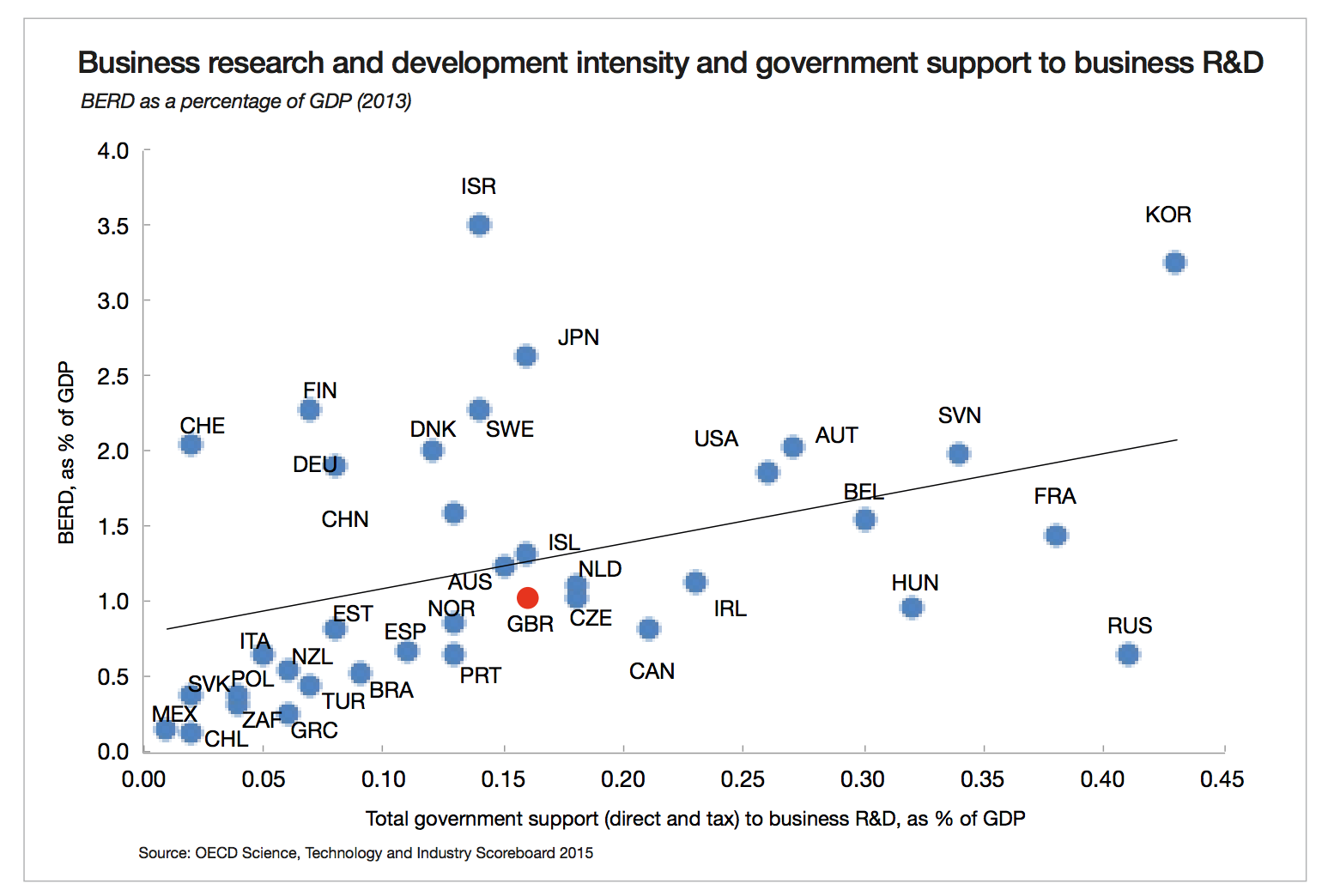

But even through the discontinuity imposed by the financial crisis, many of these themes are familiar from the Science and Innovation Framework 2004–2014 associated with Lord Sainsbury. This comprehensive and carefully thought through document had already identified one of the key weaknesses in the UK’s innovation system: low levels of business research and development (R&D) compared to competitor nations. The Sainsbury framework was brave enough to set a numerical target: to increase business R&D intensity from 1.25% of GDP to 1.7% over the decade.

Between 2004 and 2014, business R&D intensity more or less flatlined, and now, in 2017, the new Green Paper reports that “business investment in R&D (BERD) is just over 1% of GDP in the UK, close to half the rate in Germany and substantially below the OECD average”. Whatever we’ve been doing up to now, it hasn’t worked.

Something old, something new

So what elements in the Green Paper are new, and which reprise the traditional approaches?

Among the familiar themes, we have science and innovation support, including knowledge transfer, intellectual property (IP) exploitation and tax credits, skills infrastructure, government procurement, and trade and inward investment. In a return to the Mandelson/Cable tradition, support for individual sectors, like aerospace and automobiles, is specified. The question to ask here is, what will be done differently to ensure that these measures make a material contribution to the goals of the strategy: increased productivity and economic growth more spread across the economy.

To be fair, we should look carefully for measures that have worked locally, even though their impact on the whole economy may not have been enough to counter the other headwinds faced. The revival of the auto industry can be read in these terms, and this was very much a focus of the Mandelson-Cable era. Its success can be measured in overall growth of sales and exports; business R&D in the UK autos sector has also increased substantially, by 80% since 2008. One might expect this to have had a positive effect driving innovation throughout other parts of the economy touched by this sector. Overall, this looks like a success for industrial strategy, and it should be studied for wider lessons.

Many other measures may well have been sensible interventions, that in the past have simply not been done on a large enough scale to have a material effect on the whole economy. For example, over the last decade or so Innovate UK has found its feet as an agency, providing government support for industry-led innovation. But in comparison to similar agencies in other countries, it is simply too small. Perhaps its merger into UK Research and Innovation could give it a kickstart.

Nonetheless, the question we need to ask is about the absorptive capacity of our innovation system. If we were to double Innovate UK’s funding, would we find enough British businesses to lead and participate in it, given the overall low levels of UK business R&D?

DARPA envy

There has been a very substantial increase in government funding for R&D through the new ‘Industrial Strategy Challenge Fund’, announced in the Autumn Statement. By 2020, this is planned to reach £2 billion a year in scale, more than twice the size of the current largest existing research council. It is not currently obvious how or where this money will be spent.

One model that the government looks at with interest is the US defence research agency DARPA, which has a very high reputation for producing some of today’s defining technologies, such as GPS and the Internet. Is the DARPA model transferrable? Its stated goal is to produce transformational change, rather than the incremental developments that are characteristic of much applied research. But it is firmly challenge-led, instead of being defined by the priorities of any one scientific discipline.

DARPA’s success owes much to the very high calibre programme managers, who have a considerable degree of discretion in shaping projects midstream (or, indeed, terminating them, if they aren’t going anywhere). To replicate this, the UK government is going to have get past its ingrained view that the people who work for research councils are back-office bureaucrats devoted to red-tape, whose numbers should be relentlessly pushed down. Instead, the high quality people in those roles need to be appreciated for their essential contribution to the success and cost-effectiveness of the projects they are responsible for.

But above all, DARPA is very clear about what its mission is: to ensure the US military maintains overwhelming technological superiority over any rival. That clarity of mission makes it clear how its challenges are defined. The Industrial Strategy Challenge Fund needs to be just as clear about its mission, and needs to have a systematic process for setting its challenges. This needs to go beyond the traditional BOGSAT* methodology; it will take time, money, technical expertise and a diversity of viewpoints, as well as a very clear steer about strategic goals.

Spin-outs

The issue of scale applies also to venture capital. It’s a widespread complaint that the UK venture capital industry is too small, and funding isn’t available to start and grow innovative new companies. Yet if the sums available for venture capital investment were much larger (perhaps through even greater direct support from government), would there be the investment opportunities available to absorb it? Are we limited here by money, or ideas (by which I mean investable ideas, with a low enough level of technical risk and a well-developed market plan)?

Is it universities’ fault that there are not more dynamic spin-out companies being produced? UK universities are much blamed for their performance in this front, being accused alternately of over-valuing their IP, and demanding too much in return for it in terms of cash or equity stakes, or of undervaluing it and not making strenuous enough efforts to commercialise it. In fact, UK universities produce about the same number of spin-out companies, per unit of funding, as their US counterparts, so it is difficult to argue they are doing this too badly at the moment. Could we improve on how IP is handled by universities? I’m sure we could, and “identifying and spreading best practise” among universities’ technical transfer offices is always worth doing, but I doubt whether this will make an order-of-magnitude difference.

Up-skills

There are some other familiar measures that frequently get talked about, but about which, in the recent past, not much has actually been done. The shortage of mid-level technical skills in the UK is, of course, an evergreen subject (first considered by the 1887 Royal Commission on Technical Instruction), but it remains an important problem, so it is welcome that concrete measures are proposed here, in the form of a new set of Institutes of Technology.

Yet it would be a mistake to consider this in isolation. In particular, further education colleges, businesses, and universities can and should work together on intermediate level skills and training. The new Institutes of Technology would benefit from explicit links with universities to help develop “parity of esteem” between technical and higher education, to create new routes into higher education to widen access, and to emphasise the link between training and innovation.

Regional inequalities

Another very welcome new ingredient in the Green Paper is a long-overdue emphasis on the gross regional disparities in economic performance across the UK.

One very striking difference between the prosperous parts of the UK and the less prosperous parts is the degree of R&D spending they receive, both from private and public sources. The dominance of London in public sector R&D is very striking, as is its relatively small degree of private sector funding brought in to follow that. This is an issue in which industiral strategy involvement is essential, in the sense that every decision that exacerbates this imbalance must be individually justified.

For example, a £250 million national research centre for Dementia, to be hosted at UCL, was recently announced. On scientific grounds this decision can’t be faulted. UCL’s research capacity in neuroscience is outstanding and unrivalled, yet once again it adds to an overall already very unbalanced national landscape in biomedical science. So correcting these imbalances will need a long-term deliberate strategy.

Business and government/higher education R&D in the UK by NUTS 2 regions. Data: Eurostat, updated 31/03/16

Universities and the UK’s new business model

Fundamentally, an industrial strategy needs to answer the question: how is the country going to make a living? More modishly, one can express this as the need for the UK to articulate its business model and then mobilise resources – including universities – to support that.

There can be no more timely moment to do this than now, as the UK enters the process of tearing up its current trading arrangements in ways which will undoubtedly cause big shifts in the patterns of comparative advantage across the economy. We hear lots of rhetoric about the UK as a great trading nation, but trading nations have to have something to sell. The UK is a service-based economy, but as trade barriers across the world go up services will be even more difficult to trade internationally.

So if the UK is going to trade its way to success post-Brexit, it’s going to need to decide in what sectors, and in what kinds of products and services, it has the potential to be competitive and innovative in. We need to recognise that in many areas our capacity to innovate isn’t as big as it should be, and the government needs to use all the tools it has to improve that capacity, focusing not just on the supply side but on the demand for innovation as well. Some of the fundamental assumptions that governments have been making for twenty years or more will need to be revisited, because whatever we’ve been doing up to now hasn’t worked.

What is clear, though, is that there is a new urgency about industrial strategy, and this means a changed environment and new pressures for universities. Universities can and should play a key role in helping to address the UK’s productivity problem and its regional economic inequalities. This will, though, mean that some universities will need to move out of their comfort zone – just as the government is moving out of theirs – to give greater emphasis to translational research, innovation, and skills across a wider landscape.

*BOGSAT: bunch of guys sat at a table.

This article was first published on Richard Jones’ personal blog, http://www.softmachines.org/wordpress. Richard is a member of the Industrial Strategy Commission, which launched on Monday 6th March at the Royal Society.