When ministers in England respond to a question on the state of student financial support, they tend to include a reference to support on offer directly from universities.

When, for example, Robert Halfon announced his miserly 2.3 per cent uplift to the maximum maintenance loan back in January, the press release informed readers that “universities are responsible” for ensuring students who need help get the support they need, including through their own hardship funds, or through bursaries and scholarships:

I’m really pleased to see that so many universities are already stepping up efforts to support their students through a variety of programmes. These schemes have already helped students up and down the country and I urge anyone who is worried about their circumstances to speak to their university.

In fact ever since the introduction of tuition fees into England’s system, there has been an assumption that at least some of the money should be spent on student financial support over and above that provided by the national statutory schemes.

Many argue that local decision making (aka institutional autonomy) is better at designing schemes that get the money to where it’s really needed.

Others argue that redistributing fee income within a provider rather than across the country means that financial support is based not on need, but on the number of other students at your university that need it.

Who’s right?

Looking back

In the olden days, each year the Office for Fair Access (now merged into the Office for Students) would tell us, at a provider level, how many “OFFA countable” students each provider had, and how much they were spending on hardship, bursaries, scholarships and fee waivers.

It allowed us to see how generous providers were being with their “additional” (top-up) fee income, and it highlighted that the providers who did the heavy lifting on access were often the ones who could afford the least per head in student financial support.

Over the years though, direct student financial support has fallen out of fashion somewhat.

Research found that bursaries weren’t impacting applications – well no, because information on what’s on offer is so hard to find. An OFFA project found no real link between retention and bursaries between 2006 and 2011 and everyone ran the lines on that graph into this decade.

And relentless pressure to evaluate and look for impact – pressure that continues to this day – saw providers worry less about the student experience “buffer” and more about their raw entry, continuation and completion rates.

And maybe it mattered a bit less in the middle of the last decade. Inflation was stubbornly low. When George Osborne scrapped grants, he increased the value of the maintenance loan substantially.

And it’s long been the case that students studying at home – who make up a big proportion of those WP entrants – have had an accidentally more generous statutory maintenance entitlement than those away from home when considered through the optic of their respective costs.

Eventually provider-level reporting and transparency on access agreement student financial support disappeared as OfS’ obsession with outcomes allowed providers to double down on “what works” rather than virtue-signalling through expenditure.

Where are we now

The downside with all that is that we now don’t know what’s being spent – and the more the government expects universities to make up the shortfalls locally, the more we need to know.

And we absolutely need to know if universities have taken the opportunity of a different kind of regulation to hide a reduction in their expenditure on student financial support.

So to help us to understand what’s been going on, for the second year running we’ve managed to wheedle out of OfS some data under an FOI request.

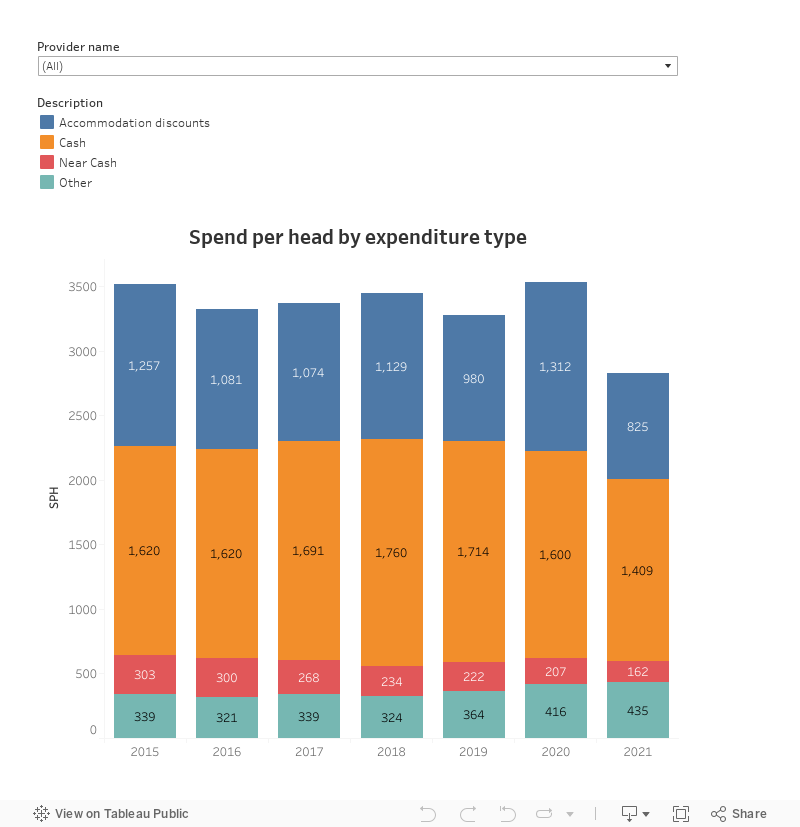

Basically, ever since the OFFA days HESA has been collecting data on the amounts of student financial support, and the number of students that helps, for each university in England – and here we have that data over the past few years.

It covers four different types of spend on student financial support:

- Cash: This covers any bursary/scholarship/award that is paid to students, where there is no restriction on the use of the award

- Near cash: This includes any voucher schemes or prepaid cards awarded to students where there are defined outlets or services for which the voucher/card can be used

- Accommodation discounts: This includes discounted accommodation in university halls / residences

- Other: This includes all in-kind or cash support that is not included in the above categories and includes, but is not limited to, travel costs, laboratory costs, printer credits, equipment paid for, subsidised field trips and subsidised meal costs

We’re not 100 per cent convinced about the data quality, this doesn’t tell us how much money is going to disadvantaged students, it doesn’t tell us about need, and it only covers home domiciled undergraduates (and below, in terms of level of study). But it is, nevertheless, fascinating. You can see the numbers for each provider in England here.

Have you won the postcode lottery?

If we just look at cash help and exclude alternative providers, last year just over £400m went to just under 300k students – a spend per head of £1,415. But dive a little deeper and you find disparities – in the Russell Group the £ per head was £2,038, but across MillionPlus providers that figure was £722.

I’m not saying that anyone’s flush with cash – but that is almost certainly an artefact of redistributing fee income around a provider rather than around a country, and appears to result in manifest unfairness.

One interesting aspect to note is that in 2019-20 the total handed out in cash was £441m, rising to £527m in 2020-21 and then falling back to £400m in 2021-22. The 2020-21 boost was almost certainly a mixture of DfE-supply of additional funding and student-pandemic related demand, but it doesn’t explain why the cash total for 2021-22 is lower than for any year we have figures for.

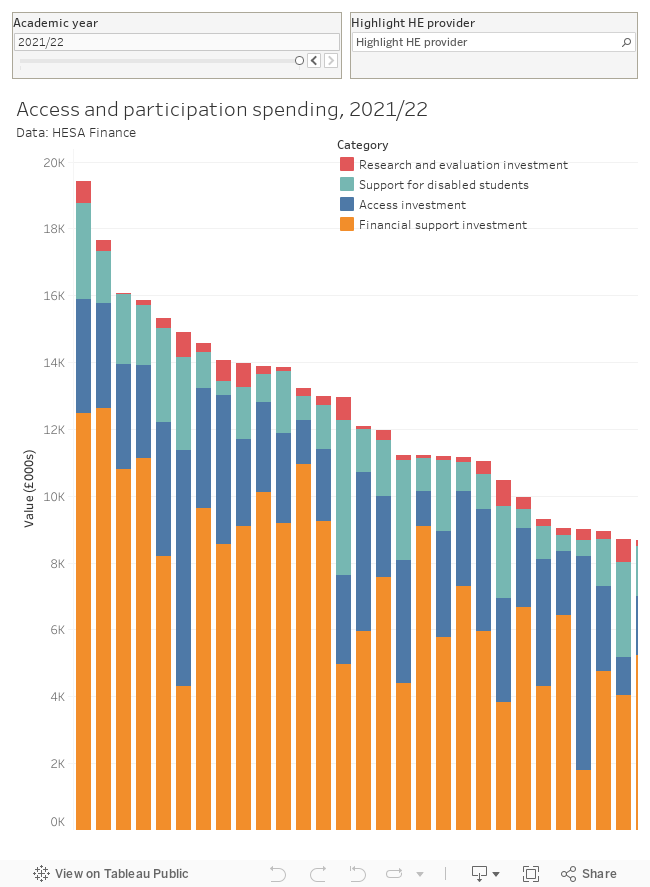

Some will point out that it might be better just to look at what’s been going on under the auspices of formal, declarable access and participation work. HESA finance data now includes a look at expenditure – but not the number of students that expenditure covers, nor the total amounts invested pre-pandemic and nor the amounts allocated in premium funding, all of which would aid meaningful comparison.

What this does all do is remind us that when ministers point students who need money at universities and say “ask them”, for whatever reason those universities are handing out less than ever – and the amount of help students will get appears to vary wildly between providers.

As long as institutional autonomy (coupled with vague expectations) trumps all other cards, we won’t really know whether any of the amounts – from an individual student award right up to the amount being spent by the sector nationally – are too much, or too little.

And if the only way to measure that is the number of students that drop out rather than the number that have an utterly miserable time and an impossibly thin, do-only-what-you-absolutely-have-to-survive student experience, the sector really is in danger of missing what matters and determining “what works”.

{kind=link}

As someone responsible in an institution for managing the team responsible for distributing discretionary financial support, whilst also providing welfare support, the biggest issue right now is that we just do not have sufficient staffing to be able to support students. The very large increase in international students has had a significant impact on demand, as has the cost of living situation, and the waiting times for each application to be assessed has skyrocketed, through no fault of my team. A large number of students have complex welfare needs (mental health, housing, lack of part time work, isolation) which require significant levels of support. Staff are stressed and close to burnout and this is having an impact on the quality of our assessment, and on the support we can provide.