Tests are great politics. Matt Hancock’s “five tests” for emerging from lockdown have an uncanny echo of Gordon Brown’s “five tests” for joining the Euro. Gavin Williamson just loves tests – they’re his favourite model of assessment.

Setting up a series of tests is, essentially, a way of refusing to make a decision based on limited evidence without the actual refusal. You set your conditions, and then wait around looking smart as reality decides whether or not to meet them. Gordon Brown never did decide to join the Euro – arguably his five tests were defined as to make this nearly impossible. We probably will, one day, return to life almost as it was before Covid-19 – it remains to be seen what benefits Hancock’s tests have in preparing for this.

I’ve been thinking about “tests” because I set two of my own the other week. For me to judge any bailout as successful, it would need to meet the following two conditions:

- It preserves sector capacity and quality

- It preserves student choice

And imagine my delight when Gavin Williamson came up with his own priorities for the sector at Education Committee (a step before “tests” to be fair):

- stability for students

- safeguarding research resources

- recognising the role providers play in local communities.

The scale of the hole the sector will find itself in is now becoming very clear, both from my work on the site and the (excellent) analysis provided by London Economics for UCU. We also now know that the Office for Budgetary Responsibility is on the case regarding the wider economic impact of a drop in international students. We are talking about multi-billion pound losses for the sector: UUK estimate £3.2bn in the 2020-21 academic year, using what to my eyes is a very optimistic set of assumptions, London Economics found a £2.5bn black hole (again optimistic) based only on changes to recruitment. My worst case scenario – with a loss of a year of income from international fees, industrial research contracts, and residences and catering – tops out at around £7.1bn, with £3.5bn at the most optimistic end. In truth, no one knows.

As we also know, large parts of the sector are in no shape to weather this kind of a detriment in one single academic year. We’ve seen large, established, universities writing to staff about the potential for 25 per cent cuts in income. There have been proposals to implement a number of bailout measures (from recruitment caps to enhanced research allocations), none of which address the scale and severity of the expected conditions next year.

My proposal

In a disaster like Covid-19, we reach for the tools that are nearest to us. The language of “business as usual” means that proposals generally start with the idea of fixes to existing processes, rather than new ideas. The temptation to fiddle with the existing system – perhaps addressing some important issues with it on the way – is huge.

My proposals come from a different place – but a recognisable one. I would suggest:

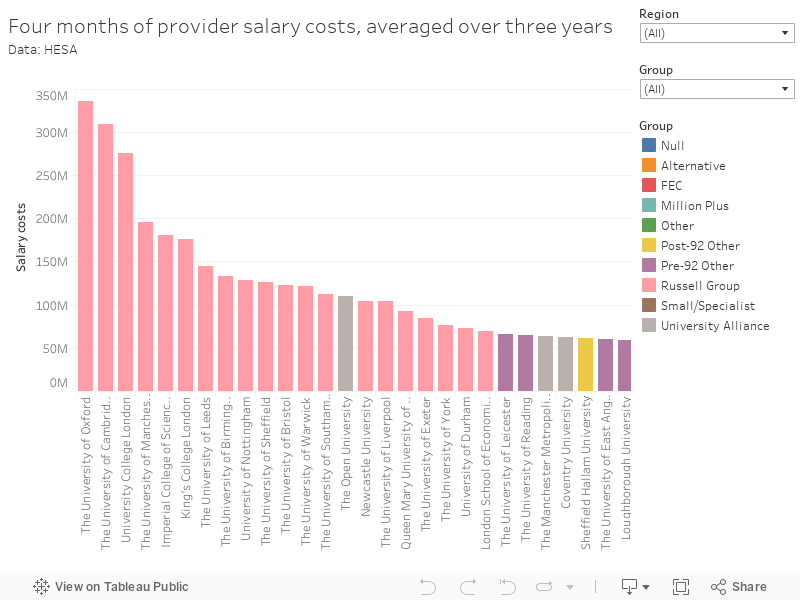

- The offer of an income contingent loan from the government, to the value of four months of the average spending on staff salaries of the last three years of operation, to every provider currently registered with the Office for Students.

- The loan is subject to an interest rate of 3 per cent plus the Bank of England base rate, from the point the loan is granted.

- It is repaid in installments on an annual basis (at a rate to be determined) from the point where income from home student fees income and OfS high-cost premium income returns to a value equivalent to the average of this income over the last three years pre-Covid. I would anticipate that at least a decade, if not two, would be allowed. Where income falls below this level repayments would pause, and providers with substantial reserves will have the option to repay immediately.

- The loans should be issued on the condition that providers commence the 2020-21 academic year in January 2021, and the 2021-22 academic year in November 2021. Providers cutting staff numbers during 2020-21 would be obliged to pay off the equivalent of 4 months salary for each staff member lost from the loan amount.

Here’s how that loan eligibility would look by provider:

Advantages

This is a true bailout in the traditional sense. It addresses a particular and identifiable gap in outgoings (salary costs), not income. As a large part of most universities income is derived based on student choice, replacing or supplementing this income involves the prediction of prospective student choice based on next to no data.

The loan aspect avoids moral hazard. Providers can repay annually, with interest, or choose to repay the balance early using reserves or other borrowing. A bailout is provided for the impact of an externality, not because of a failure of management. Those providers that have built up significant reserves could repay the loan early, thus saving money over the long term.

Vice chancellors like to say that the value of the university is in its staff – this proposal preserves this value of this asset during a period where normal business activity is difficult or impossible. In doing so we preserve student choice – assuming recruitment post-Covid-19 for January has a passing similarity to usual patterns there is no need for the sector to radically change size or shape only to deal with a return to growing student numbers from home and overseas in years to come.

Staff numbers would remain static. Providers would not be tempted to lay off staff and bank the savings, as funding commensurate to the loan for each salary would need to be repaid immediately – although the option would remain if they thought the overall saving was greater than the immediate detriment.

The configuration of the funding as a loan significantly lessens the impact on government borrowing, as an income stream is now attached to it. Changes to the way income contingent student loans are treated in the national accounts would apply only to a limited extent – all registered providers will have passed condition D1 and the loan does not have a write-off as student loans do so no RAB charge would apply.

The deferral of the start of the academic year has been proposed several times, but the benefits are worth restating. It would allow:

- Prospective students the chance to sit an A level exam should they so wish, and to be assessed for practical/vocational elements of other courses.

- Prospective and existing students space to recover mentally from the huge stresses that Covid-19 has placed them under. The school-university threshold is hard work at the best of times, this year would have been far worse. A pause would help all those involved return in January with the capacity for academic work.

- Providers chance to develop new course portfolios that meet specific economic and structural needs for the UK. Alternate delivery modes, such as part-time or accelerated courses, or workplace delivery, could be set up.

It is very likely that higher than usual volatility in home and international recruitment would be mitigated in part. Prospective students will behave differently, in ways we cannot currently predict, but behaviour four months after lockdown ends (for example) will be different than behaviour four days after lockdown ends.

The shorter deferral in 2021-22 would allow space for the usual break between academic years – allowing more time for resits, module and programme boards, graduation ceremonies (for this year and the previous year?) and all of the other work that traditionally takes place during the summer.

Disadvantages

The initial outlay would be eyewateringly expensive. Assuming this is limited to providers who are both registered with the OfS and returned 2018-19 finance data to HESA, we’re looking at slightly under £6bn. Though almost all of this money would be repaid over time (and indeed, slightly more, given the interest rate), it represents a significant initial commitment that I could imagine would raise eyebrows in the Treasury.

But compared to the £40bn estimated cost for three months of furlough (which will never be directly repaid), plus the spending on other aspects of the Covid-19 support package (upwards of £175bn, most of which will never be repaid), it is not entirely out of the ordinary. Especially given the wider impact of the higher education sector on the economy.

The treatment of the sector is out of line with other sector bailouts. The tendency has been to try to replace or mitigate changes in existing income streams – not to replace expenditure. But the time-based impact on the sector makes things different. We know that a crunch is coming, as opposed to finding we are already in a crunch. We also know that the best mitigation is to delay the start of the academic year – a pause until January could well return fee income almost to existing levels.

Covering staff salaries neatly preserves research capacity, and preserving providers in this way means that student choice and wider local impacts remain intact. However, the availability of loans would be disproportionate across the sector – the Russell Group would see far more funding than other providers. Presentationally this doesn’t look great, although the fact that expenditure is being met does justify the differential.

Replacing salary costs would also reopen the senior staff pay argument. You could imagine a tweak to this idea that excludes VC pay, or a voluntary agreement for VCs not to take their full pay during the furlough period the loan covers. It feels a bit vindictive – especially given the stress VCs have been under and the minuscule contribution of VC salaries to expenditure – but it would be a good populist move.

We would be relying on providers that franchise out provision to support the institutions they send students to. We also don’t bail out providers that are not registered with OfS. In both cases the availability of general bailouts (specifically those focused on SMEs, a category into which most alternative providers fall) would help, but it is still a blind spot.

And not all salaries linked to universities are shown in the data under staff salaries. Outsourced staff (for example the key workers that maintain and clean university estate) would not show up in the fields I am looking at. For very different reasons, neither would students’ union staff. Both – and other examples – are key to running a university: providers and SUs would need to meet these costs from elsewhere.

How could it happen?

This proposal meets Gavin Williamson’s tests, and mine. It is a big initial outlay, but while borrowing costs are low and the appetite for borrowing is there it isn’t insanely so. It is kinder to current and prospective students, and kinder to university staff. By addressing actual costs (which are largely uncontroversial) we avoid the inequalities embedded within existing allocations.

Funds would flow through existing payment processes via either OfS or the Student Loans Company. I’d actually tend towards the latter as they could also handle the repayment aspect using the systems they currently use with students. There’s very little danger of providers failing to repay the loans, in time – demand for UK higher education has grown at home and internationally since 2012, and it is unlikely that this trend would not continue given the rise in the number of UK 18 year olds over the next few years.

And what will universities do with full staffing and no students this autumn? There is a lot of work to do in terms of work with the local community, with industry, and with government to address the economic and social impact of Covid-19. There are plenty of students who need to catch up that we couldn’t quite cater for this term. There is a lot of work to do to prepare courses to support the “new normal”, and to offer online professional development and support to key workers. Universities are perfectly placed to help.

It’s an investment in sector capacity, after all. This capacity can be used in a number of ways, but once lost cannot be easily replaced.

It’s clear and simple to defend. I particularly support delaying the start of the year until January 2021 (full disclosure, I have an 18 year old daughter) and I would like to see it backed up with a national volunteering programme (some version of the NCS?) so that those students have the opportunity to contribute as well as it providing structure and purpose for those months when all of the usual “gap year” activities, as well as the opportunity for paid work, are likely to be heavily constrained.

Interesting idea but worth thinking through what current (undergraduate) applicants would be doing in autumn 2020 – or how they’d support themselves. Worth noting that DfE and Ofqual stuck to the A-level and BTEC certification timetable in summer on the assumption that this was better than a hastily arranged set of autumn exams.

One possible obstacle to lending more money to institutions are the conditions written into existing loan arrangements (covenants). A few years ago government accountants (in BIS/BEIS) decided that short-term advances to FE colleges needed to be handled like proper loans with proper contracts and all that. This created a stand-off with existing lenders who insisted on complex inter-creditor agreements to protect their interests – keeping the bank ahead of the government in the lending queue. This isn’t a directly comparable situation but students, staff and OFS ren’t the only stakeholders. Banks, pension funds (USS, LGPS) and suppliers also have interests which they might act to protect.